What will it take for Pakistan to deliver on its investment climate goals

It was never a macroeconomic problem. A six-year account of governance, capture, and the reforms no one in office will table.

In 2020, I began a national assignment to reform the regulatory landscape of Pakistan. Pakistan inherited most of that landscape from the British Raj. When the British left, instead of reviewing and removing rules that fit neither the era nor the realities of what was now Pakistan, successive administrations added to the swamp.

The regulatory creep only grew. Unlike India, which dismantled the licence raj in the 1990s, licences and licenses doing as quasi-taxes, registrations, NOCs and other similar instruments in Pakistan kept multiplying, because they fed the corrupt bureaucratic system that profited from them.

Take the arms license. Issued for up to five years with a heavy renewal fee, acquiring one meant several visits to the Commissioner’s office, where your application landed in a heap. Weeks passed. Then someone would explain the right way to “expedite,” which involved cash changing hands under the table. The amount decided how long the license took. Licences became alternate income streams for the bureaucracy, the single point of failure in Pakistan’s progress. If the aim was gun control, registration at the point of sale would have done the job. A police verification and fitness test could have solidified it would not be used for law breaking. If the aim was revenue, an import tariff would have sent the money to the state rather than to a baabu whose one accomplishment in life was passing an exam that handed him these privileges. The license did nothing to stop criminals, mafias, and terrorists from buying and using weapons. It is one example among many of how the bureaucratic machine enabled the scope creep of regulation.

The 18th Amendment and the devolution that followed only made things worse.

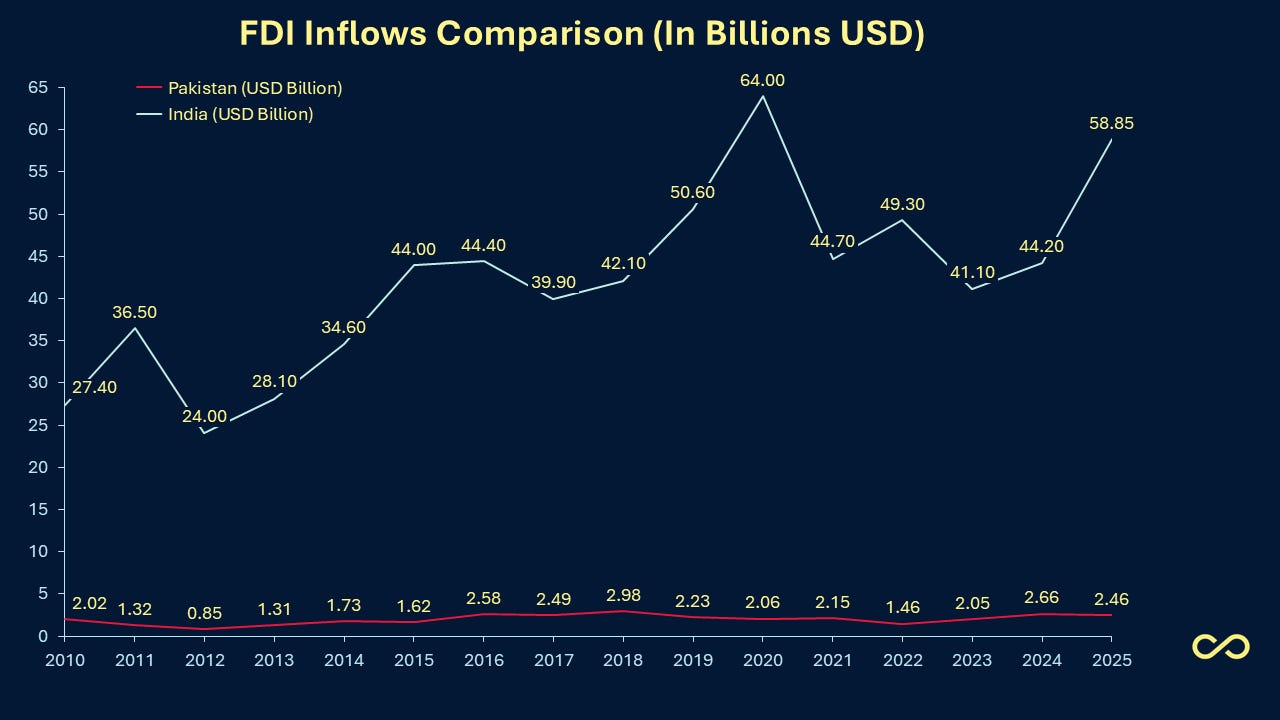

The results have been heavy. An exodus of Fortune 500 companies, a decline in foreign direct investment, and a fall even in local investment.

In 2020, when I got a seat at the big table to fix this, the work led to a whole programme, the Pakistan Regulatory Modernization Initiative (PRMI), and gave me the chance to write its Strategy and Implementation Plan (It is supposed to be housed in the link shared but surprise, the website is down!).

Six years later, that plan still sits unimplemented.

I came to a conclusion early: the problem was not macroeconomic, it was a problem of governance. Until the bureaucratic system, which behaves like a cartel, was taken apart, nothing would change. That conclusion held.

Six years on, the Board of Investment, the body charged with carrying out the initiative, did what every other layer of Pakistani officialdom does. Roadshows. Workshops upon workshops. Photo ops. Paper pushing. And constant delay of the actual objectives.

Someone, perhaps, noticed, and so SIFC was created in 2023. In September of that year I was deputed via FCDO’s technical assistance under their governance programme to SIFC as a consultant, helping set up its cadenced implementation, tightening committee meetings, and trying to keep it from stalling at the point of execution.

The aspiration behind SIFC was honest.

Three years on, it too appears to have missed its annual targets. Why? Because the ears at SIFC stayed tuned to the same bureaucratic music: committee meetings spent on paper pushing, on shuttling opinions from one ministry to another, all of it sheltered behind the Rules of Business 1973 and its tangled logic.

The bureaucrats, in effect untouchable because they cannot be removed, spent time, resources, and a rare chance the country had to fix its socioeconomic predicament.

This piece sets out what I saw, what the data said when I drafted PRMI, and what it would actually take to break the pattern.

The picture in 2020

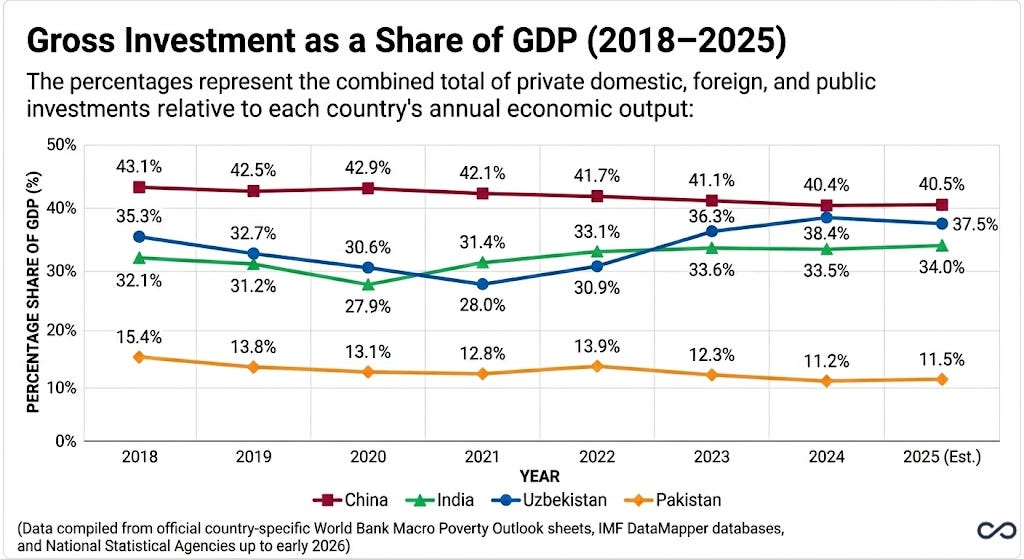

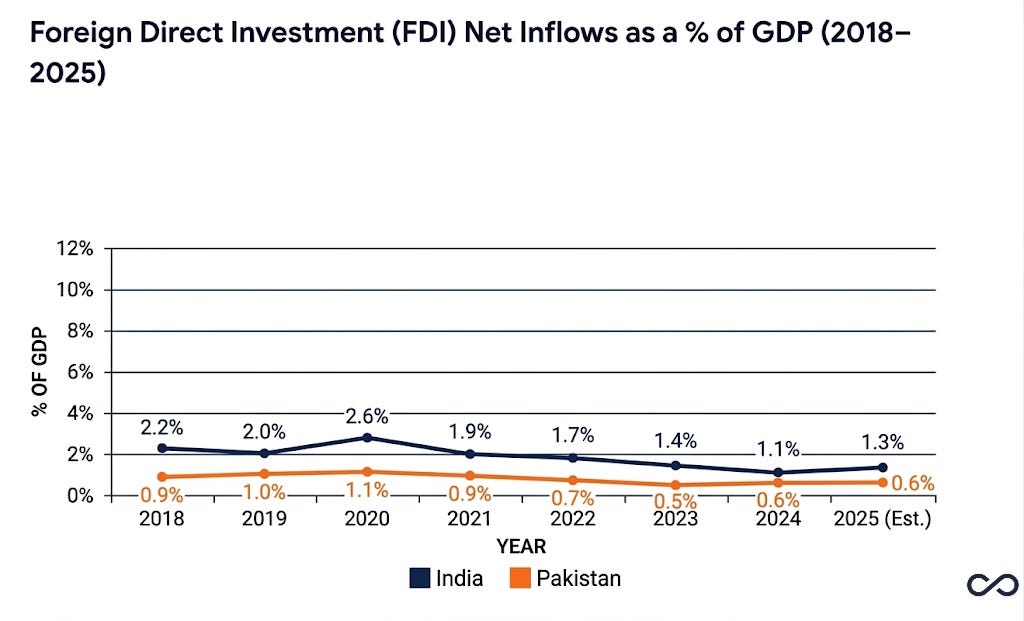

When I wrote the PRMI problem statement, the numbers told a plain story. Private investment in Pakistan stood at 11 percent of GDP. India sat at 29.1 percent, China at 35.2 percent, and Uzbekistan at 21.2 percent (World Bank, 2018 and 2019). FDI into Pakistan was 0.9 percent of GDP, against 1.7 percent in India, 0.99 percent in China (excluding Hong Kong and Macao), and 4.1 percent in Uzbekistan (UNCTAD, 2019).

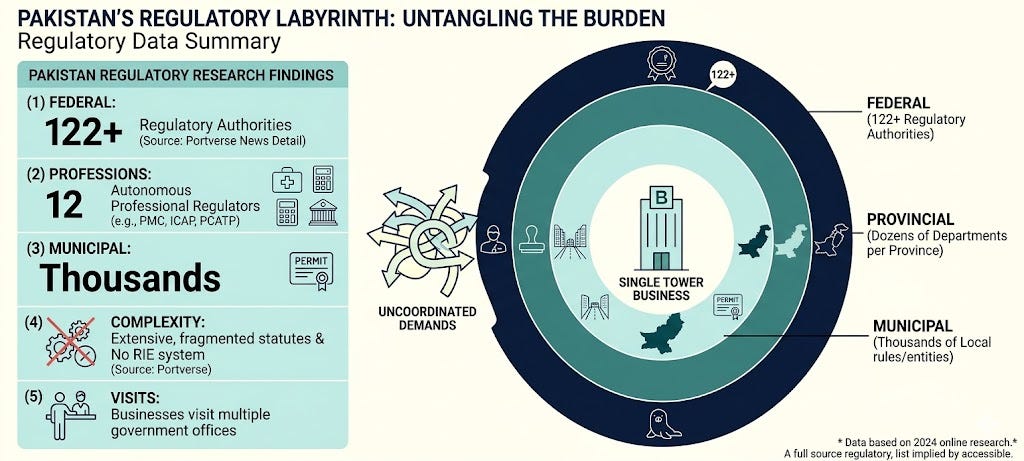

The private sector pinned the blame on regulation. Dealing with registrations, licences, permits, and certificates in Pakistan was costly and overlapping across federal, provincial, and municipal lines (IFC Country Private Sector Diagnostic, 2021). Over 100 federal, provincial, and local agencies regulated business activity, each acting on its own.

The damage was sector-wide.

The cost showed up first in the two priority sectors the government and IFC had picked, automotive and pharmaceuticals, but the same regulatory paralysis spread across the economy.

In autos, the plan to push parts exports from $70 million to $1 billion and to electrify 30 percent of cars by 2030 stalled. Around 500 tier-1 suppliers stayed stuck on plastics, trims, and tyres, while drivetrains and engines came entirely from abroad, because local firms lacked the scale and technical help for high-cost precision work. Outdated EURO-II emission rules and the absence of basic safety standards locked Pakistani parts out of export markets, and labour productivity sat at a reported 30 to 50 percent against training that taught nothing of advanced methods.

In pharmaceuticals, the goal of growing exports from $300 million to $5 billion by 2025 ran into a web of over 51 federal, provincial, and local agencies (DRAP, the Anti-Narcotics Force, the Federal Board of Revenue, provincial health departments, and municipal bodies), where a single drug-price increase could take eight to twelve months to clear Cabinet. With prices fixed while the rupee fell, bringing new molecules to Pakistan became unviable, which drove out 12 multinationals in 2017, pushed another 24 to cut capacity, and left the sector around 95 percent dependent on imported active ingredients.

Information technology faced a different absurdity. The bureaucracy tried to govern software houses with production-era factory and worker-safety laws, letting inspectors penalize or seal IT firms. The Federal Board of Revenue kept serving tax notices even after the government announced income-tax exemptions for the sector, forcing firms to fight legal battles they should never have had. Restrictive foreign-exchange rules made it hard for freelancers and small firms to collect overseas payments, choking grassroots digital exports at the source.

Agriculture and food processing drowned in geography. Punjab ran 135 separate market committees and Sindh 71, so a food business that shifted jurisdiction or bought from a new area had to apply for a fresh license and certificate each time. On exports, the state never set up a single Foot and Mouth Disease free zone recognised by the World Organization for Animal Health, which alone blocked commercial meat exports to developed markets.

Tourism and mining hit the constitutional wall. Both became provincial subjects after the 18th Amendment, with provinces often refusing to cooperate on land and mining licenses, and No-Objection Certificates.

Logistics, ports, and shipping stayed paper-bound despite the Web Based One Customs system. When a vessel docked, businesses still had to hand physical documents to different departments, each demanding its own set of photocopies. Without a true electronic single window, delays piled up and supply-chain costs rose.

Textiles and leather, the largest export sector at over 60 percent of exports, took the energy hit hardest. Power shortages cut production by a reported 20 to 30 percent, forcing firms onto costly backup generators and pricing them out of global markets. Compliance certification for safety and environmental standards stayed riddled with corruption, and because major buyers avoid firms that breach child-labor and safety rules, Pakistan stayed shut out of higher-tier value chains.

The pattern repeated across all sectors. Manual processing, overlapping federal and provincial mandates, and outdated laws applied to modern industries.

The problem was never the sector. It was the system regulating it.

The PRMI objective was simple to state and hard to do: raise private investment by cutting compliance costs, automating procedures, fixing standards, and adjusting incentives.

In 2022, after two years of sweat and toil, PRMI was launched in an extravagant ceremony at the Presidency. Its implementation plan published and distributed. More photos taken. A letter of appreciation handed. I wish I could write more concerning its tangible impact.

PRMI became a named pillar of the Pakistan Investment Policy 2023, designed to cut unnecessary Registrations, Licences, Certificates, and Permits.

It stalled for the reason these efforts almost always stall: the plan was handed to the same bureaucracy that profits from the bottlenecks.

Asking a ministry to review and shrink its own rule book is asking a tollbooth operator to remove the toll.

My PRMI Strategy and Implementation Plan proposed a regulatory guillotine and sunset clauses. The guillotine put every rule on trial at once and abolished any that could not be justified. Sunset clauses gave every rule an expiry date, especially those that predated Pakistan’s independence, so survival had to be earned on merits of protecting human, environmental and national security. The Standard Cost Model would put a rupee-and-hour price on every compliance burden that would remain. And a fully digital Pakistan Business Portal would act as a virtual single point of entry, taking the humans out of the middle. These foundational measures were designed to shift the burden of proof off the citizen and onto the regulator.

None of these were put into force.

Today, the plan I drafted in 2020 reads like a description of what is still missing. That is not a comfortable thing to write about one’s own work.

The reforms it set out, killing the manual processing of Registrations, Licences, Certificates, and Permits (RLCOs), ending overlapping jurisdictions, and stopping arbitrary enforcement, were never taken apart at the root. They were adopted in name and starved in practice.

On paper, the Pakistan Investment Policy 2023 folded PRMI in officially. The Board of Investment, as the designated lead agency, ran stakeholder feedback and a review of existing RLCOs across federal, provincial, and district levels. The Securities and Exchange Commission digitized company registration, and a Branch and Liaison Management Information System and an SEZ Management Information System were stood up. A National Steering Committee was sanctioned to map and review the stock of RLCOs.

The pieces that would have hurt the bureaucracy were bypassed.

The independent National Regulatory Delivery Office, meant to institutionalize reform by 2022 and take it out of the hands of the regulators it was policing, was not built.

The guillotine that would have cut the stock of red tape was not fired.

The Pakistan Business Portal that would have removed face-to-face discretion by 2023 did not replace the manual workflow.

Three accountability questions still have no public answer, and whoever picks this up should ask them on day one.

First, where is the Standard Cost Model baseline that was due by September 2021? Without it, nobody can state in rupees what six years of inaction cost the private sector, which is conveniently how the people responsible prefer it.

Second, what became of the roughly $10.6 million (about Rs. 1,600 million) earmarked for consultancies, project management, and the portal? Disbursed, idle, or quietly re-routed when the timeline slipped?

Third, did any province launch the proposed regulatory sandbox districts, and with what result?

The silence on all three is itself a finding.

What the reforms would have been worth

The plan set a medium-term target of cutting the regulatory burden by 30 percent. In the simulations I ran back then, a 25 percent cut in administrative burden produced an initial rise in GDP of around 1.1 percent and a long-run real GDP gain of 1.4 to 1.7 percent, through higher savings, investment, and capital build-up.

Separately, moving from the 75th to the 25th percentile on the cost of starting a business was associated with faster GDP growth in naturally high-entry industries, with the cited range running as wide as 25 to 50 percent a year in those specific sectors.

This was the prize that was left on the table.

Six years after the diagnosis, the scoreboard is mixed, and honesty requires saying so.

The United States State Department’s 2024 Investment Climate Statement recorded that the Board of Investment introduced PRMI in June 2021, and that as of April 2024 only one project, the Reko Diq mine run by Canada’s Barrick Gold, had been designated a qualified investment under the new facilitation regime.1 One qualified project in roughly three years is a thin return for the apparatus built around it. The same report describes an economy that came close to default in June 2023 and leaned on a $3 billion IMF Stand-By Arrangement from July 2023 to April 2024 to stay afloat.1

The honest reading: the patient stopped bleeding, the underlying disease was managed, not cured.

Enter SIFC: single window, or the seventh door?

SIFC was sold as a single window to skip the red tape and pull approvals into one place. The structure tells a different story.

Pakistan already ran six other overlapping investment bodies. SIFC added a seventh layer of intent on top of a system already broken into pieces. Investors now read mixed signals from seven directions.

I watched the mechanics from inside. You would arrive at SIFC. A coordinator would connect you to another coordinator, who would connect you to someone in a line ministry, who would refer you back. You ended up circling dozens of staff and landing nowhere.

This is the one place where digitalization could have done real good.

A chatbot, a rules engine, an automated case tracker, anything that cut the human handoffs, would have removed the very friction SIFC was built to remove. None of it was built in earnest.

Three more problems sat on top:

SIFC could not force a province to comply on a devolved subject.

Speed over care. In a hurry to show wins, SIFC reportedly cleared several mining licences in Balochistan without the required Environmental Impact Assessments, which fed local opposition and echoed the early errors of CPEC.

A poor governance verdict from outside. The IMF, in its comprehensive Governance and Corruption Diagnostic Assessment, warned that SIFC lacked built-in transparency and questioned the sweeping powers and immunity granted to SIFC officials under the Board of Investment Act, arguing that overlapping mandates and opaque regulatory relaxations weaken governance.

Ultimately, the SIFC’s fundamental flaw was that it attempted to apply a process improvement to an entirely unreformed system. No amount of facilitation could compensate for the broken institutional foundation.

A governance problem wearing a macroeconomic mask

The answer to why PRMI failed, and why SIFC has not been able to solve the problem it was created for, and why Pakistan in general fails to attract private investment points to one problem: governance in the hands of an archaic bureaucracy doing more harm than good.

Pakistan does not fail to attract serious FDI because of exchange rates or inflation alone. It fails because of how the state is run. Four problems feed each other.

The generalist bureaucracy.

The Central Superior Services (CSS) and the Pakistan Administrative Service (PAS) sit at the centre. This is a colonial-era jack-of-all-trades model. Officers rotate so often that expertise never builds. One 2025 PILDAT institutional review reported an average tenure of about 2.4 years in federal ministries, and fewer than 15 percent of federal secretaries holding advanced technical qualifications in the portfolios they ran.

The effect is a 21st-century economy managed by an 18th-century administrative habit.

Constitutional friction.

The 18th Amendment devolved power to the provinces, but the centre kept trying to steer investment through national bodies. Tourism, agriculture, and minerals are provincial subjects. So a federal body like SIFC has no legal power to order land acquisition or issue environmental No-Objection Certificates.

State capture.

The vacuum gets filled by elite capture. Politically connected families, cartels, bureaucracy which enables them and in turn benefits from them, hold large parts of the economy. They use manual licensing and frequent Statutory Regulatory Orders (SROs) to protect monopolies, which keeps foreign competitors out.

The wrong kind of money.

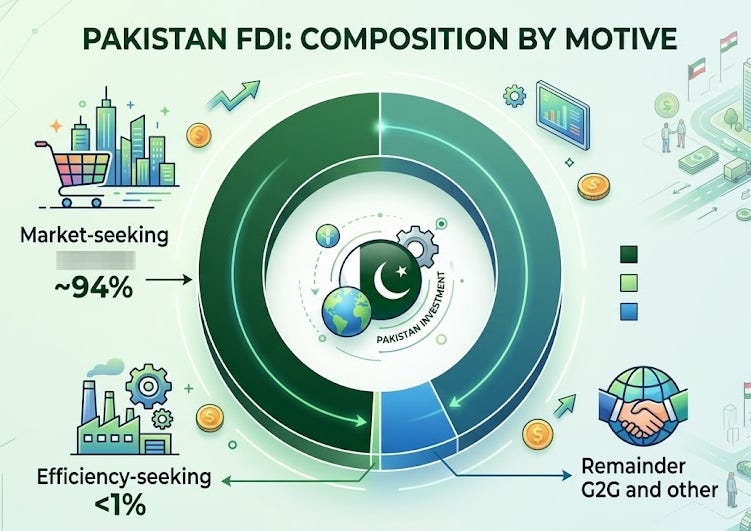

Because of all this, Pakistan attracts almost no efficiency-seeking FDI, the kind that lowers production costs and plugs a country into global value chains and exports. Data from the State Bank of Pakistan and the International Finance Corporation indicate that roughly 94% of FDI in Pakistan is market-seeking, aimed at domestic consumption in protected sectors such as power and telecom. Efficiency-seeking investment, which drives exports, represents less than 1% of total FDI, with the remaining capital heavily reliant on government-to-government inflows from China and the Gulf.

This is the trap. Market-seeking money does not build an export economy. It rents the consumer base and goes home with its returns.

The governance conundrum, rooted in bureaucratic corruption and driven by a non conducive political economy and elite capture becomes a key reason for why investors prefer men in uniform - no matter how unpopular this sounds.

Dictatorial periods in Pakistan drew 52 to 63 percent higher FDI than democratic ones, holding other factors equal.

The reason is worth sitting with, because I am not building a case for military rule.

Investors value predictable, centralized authority over a process that keeps reversing itself.

Under elected governments, the bureaucracy is politically tied. Officials help politicians win, and politicians reward them with the postings and perks they want. A large share of today’s federal secretaries rose through that exchange.

Under a military setup, the chain of command at least pushes decisions to a close. Pakistan needs an investment system that decides and sticks, whoever is in office.

How other countries broke the same wall

None of this is unsolved. Several states started where Pakistan is and got out.

Vietnam (Doi Moi) split day-to-day administration from policy expertise, brought in subject-matter specialists, and opened up foreign-investment law. It climbed from 77 to 55 in global competitiveness rankings, and high-tech goods reportedly reached 42 percent of export value.

India skipped piecemeal tinkering. It folded 13 central labour laws into a single electronic system, issued nationwide licences, and added deemed approvals for small firms, so a non-response from a bureaucrat counts as a yes.

South Korea ran a “cost-in, cost-out” rule. No agency could add a new regulatory cost without removing an existing one of equal or greater burden. It paired this with a regulatory guillotine that reportedly halved the number of registered regulations.

Bosnia and Herzegovina set up a “Bulldozer” committee of private-sector leaders and international bodies that went around the standard bureaucracy and pushed through 50 targeted reforms in 150 days.

Mexico used a “skunk works” model, placing a small technocratic unit (the UDE) at the centre of government, outside the normal bureaucracy, to force deregulation past the officials who would otherwise block it.

The common thread across all five: none of them asked the bureaucracy to reform itself.

Each one changed the default rules, moved authority outside the affected offices, or both.

The paradox no one wants to name: who holds the pen

Remember, the people who draft the reform summaries and ordained to implement them are the same people who lose their monopoly if the reform passes.

The Pakistan Administrative Service (PAS) previously known as the District Management Group (DMG) of the civil services, works as the gatekeeper of state power. Any move to digitize or open senior posts triggers what one can fairly call an institutional veto, and the reform arrives dead on arrival.

Even Britain, which built the colonial steel-frame model, abandoned it decades ago. Pakistan’s version stayed frozen.

So how do you bypass a veto held by the people writing the rules?

The honest answer follows from one observation, applied with a razor: whoever controls the file controls the outcome. Take the file out of their hands.

And this requires taking aggressive measures without wimping out. Below, in my opinion and experience, are measures without which the macroeconomic vision for Pakistan will never be achieved.

1. Abolish the PAS, do not reform it.

Every plan so far tries to coax the Pakistan Administrative Service into change.

The Pakistan Administrative Service controls the federal and provincial governments through the Rules of Business 1973. These rules dictate that the Establishment Division manages all civil service postings. This structural design creates a closed loop of authority.

The bureaucracy maintains its hold through three main mechanisms:

Generalist Control: Officers from the Pakistan Administrative Service occupy the top grade BPS 22 positions across all ministries. They manage specialized sectors like health, technology, and industry without subject expertise.

Blocked Entry: The bureaucracy actively prevents the entry of private sector specialists into senior government roles to protect internal promotion pipelines.

Resource Capture: The system secures extensive financial benefits for its members. The total federal pension liability reached Rs 1.055 trillion in the 2024 to 2025 budget.

Therefore, the cleaner move is a constitutional amendment ending the All-Pakistan generalist cadre and rebuilding the senior civil service from zero on fixed-term, sector-specific contracts. You do not negotiate with the gatekeeper. You remove the gate.

2. Carve out charter jurisdictions under foreign commercial law.

Investors require a predictable legal framework. You can provide this certainty by modifying the existing Special Economic Zones Act of 2012.

A workable reform involves three legal changes:

Statutory Autonomy: Amend the law to remove the Special Economic Zones from the purview of the Establishment Division. Staff the zone authorities entirely with private sector specialists on contract.

Dedicated Commercial Benches: Create specialized commercial courts within the existing provincial high courts. Staff these benches with Pakistani judges who have extensive corporate law backgrounds.

Binding Arbitration: Mandate that all disputes default to international arbitration under the New York Convention. Pakistan has ratified this convention. This guarantees foreign investors legal certainty using existing international treaties.

3. Outsource the sovereign chokepoints.

Hand customs clearance, certain tax collection, and one-stop licensing to international firms on performance contracts with hard penalties. Several states have run customs through external agents when the home service was captured. It is an admission that the state cannot do the job, which is exactly why it works: the contractor has no pension, no posting cycle, and no cartel to protect.

4. Stop regulating where a credible foreign regulator already has.

Auto-accept US, European, UK, and Japanese certifications for pharmaceuticals, auto parts, and medical devices instead of duplicating them through domestic bodies that add delay and a bribe point. If a drug clears the US or European authority, it clears Pakistan by default. This guts a whole class of discretionary licences at a stroke.

5. Use the military’s execution capacity inside a hard time limit.

The fact that in Pakistan investors historically favoured centralized, predictable authority, is uncomfortable but informative. Rather than pretend it away, cage it. Grant SIFC a defined execution window, say 6 to 18 months, with power to clear approvals, then a legislated hard handover to a civilian regulatory office

6. Kill the macro uncertainty.

A hard currency board, or partial dollarization for trade and investment accounts, would remove the exchange-rate and policy-reversal risk that scares off long-horizon capital. No facilitation can compensate for a currency investors do not trust.

7. Sell residency and citizenship for investment.

Gulf golden-visa and Caribbean citizenship-by-investment programmes price a passport and a residency permit and bank the proceeds. Pakistan has the consumer base and the diaspora pull to do the same, and the revenue is immediate. The recent diplomatic gains support this.

8. Buy provincial consent rather than fight the 18th Amendment.

The constitutional deadlock will not yield to federal bluster. Offer the provinces a guaranteed share of project revenue and full transparency in exchange for ceding a single, binding investment approval, with deemed approval if they sit on a file past the clock. Make cooperation pay more than obstruction.

9. Pay the top tier private-sector money, strip their tenure entirely.

End the bargain where a bureaucrats cannot be fired. Replace it with high salaries that match the private market and at-will, performance-linked terms. Security of tenure is the asset the cartel actually protects. Take it away and the incentive to obstruct collapses.

10. Make reversal expensive and visible.

Lock the changes in through ordinances, legislations and notified SRO repeals, so undoing them requires a deliberate, public act rather than quiet inaction. Reform that can be reversed by a memo will be.

11. Anchor it to an outside commitment.

Tie the package to an external condition, such as an IMF programme benchmark, so the political cost of backsliding lands on the government from outside. This gives the head of government cover to hold the line when the bureaucracy pushes back.

A closing word

I spent six years inside this. I helped develop PRMI, supported the setting up of SIFC in 2023 , and watched both get absorbed by the system they were meant to fix.

A service that profits from delay will produce delay, however many roadshows it hosts. The way out does not run through better workshops. It runs through changing who holds the file and what happens when they sit on it.

The plan that would have prevented much of this was written, costed, and ready in 2020.

It fails for want of someone empowered to run it without first asking permission from the people it strips of power.

Give that authority to the right hands, with the leeway to bypass the gate rather than knock on it, and the timeline shortens from a decade of workshops to a handful of months.

Withhold it, and the next acronym will fail the way the last two did.