Weekly Brief | Week of June 10, 2026

The Gulf’s Margin Call: How UAE and Geopolitics Are Squeezing Pakistan

This brief follows a long hiatus. The disappearance was deliberate and concluded with the launch of a wellness startup that I was actively supporting and invested in, as well as the completion of several upskilling activities that had been on hold for some time.

The Bottom Line

Pakistan’s fiscal fragility and its western insurgency are the same vulnerability seen from two angles. A state that owes 51 paisa of every tax rupee to creditors cannot fund the security response that would settle the Gwadar question. The actors who gain from Gwadar failing understand this. The budget and the Balochistan war are not two stories. They are one exposure, and Abu Dhabi, New Delhi, and Tel Aviv can read a balance sheet.

The new budget sets a 15.267 trillion rupee tax target and reserves 7.824 trillion rupees for debt servicing before a single school or road is funded. The economy grew 3.70 percent, the fastest in four years, yet poverty stands at 28.9 percent. The growth is import fed, which means it spends the very dollars the state is struggling to hold. While the books strain, Islamabad has taken on the most exposed diplomatic job in the world, brokering talks between the United States and Iran. That role has won praise in Washington and punishment from Abu Dhabi. The state is running two high wire acts at once, fiscal and geopolitical, and a fall from either rope ends both.

How to read the confidence calls in this brief

I assign rough probabilities to the load-bearing judgments so you can weight them yourself rather than take them on faith. High confidence means above 70 percent. Moderate means 40 to 70. Low means below 40. Where I cannot price a claim from open sources, I say so.

The assumptions this analysis rests on

Three assumptions carry the weight of everything below.

First, the UAE-India substitution is settled rather than reversible, meaning Abu Dhabi has decided India serves its interests better than Pakistan and will not walk that back if the regional temperature drops.

Second, Taliban tolerance of Baloch Liberation Army sanctuaries is a choice rather than an accident of weak border control.

Third, the current ceasefire between Washington and Tehran holds through the budget cycle. The third assumption is the fragile one. If the ceasefire breaks, the fiscal projections in this budget would require an immediate reevaluation.

How Will The Next 60 Days Look Like

The pressure lands on the people least able to dodge it. Documented businesses and salaried workers carry the new tax target because they are visible to the taxman while farms, shops, and property deals are not. That is a political choice, and it has a price.

Squeeze the only people who already pay, and you teach everyone else that registration is a trap.

Unrest is a high probability. The Tehreek-e-Taliban Pakistan threat in Khyber Pakhtunkhwa is active, instability runs through Azad Jammu and Kashmir and Balochistan, and the military is conducting daily counter-insurgency operations. The security apparatus has no slack left.

Abroad, everything hangs on a fragile ceasefire between Washington and Tehran. Pakistan imports 85 percent of its fuel from the Middle East, so a collapse in talks travels from the Strait of Hormuz to a Karachi kitchen in weeks. Fuel goes up, transport goes up, food goes up, and the street responds. The finance and interior ministries need flawless execution for two straight months. Neither has a record of it.

What Has Changed Or Is Changing

The Pakistan Economic Survey 2025-26 survey describes one country splitting into two economies.

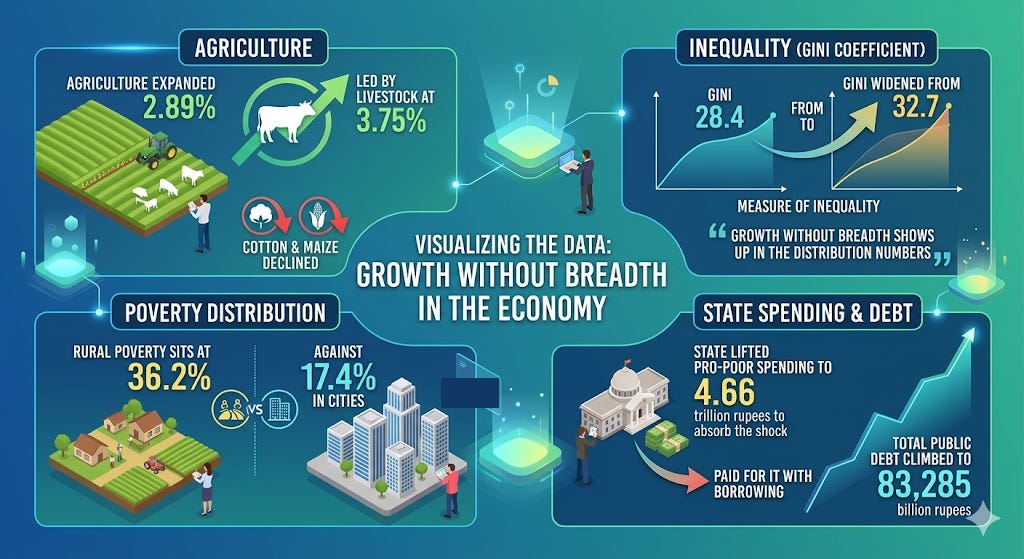

Agriculture expanded 2.89 percent, led by livestock at 3.75 percent, while cotton and maize declined. Growth without breadth shows up in the distribution numbers. The Gini coefficient, a measure of inequality, widened from 28.4 to 32.7. Rural poverty sits at 36.2 percent against 17.4 percent in cities. The state lifted pro-poor spending to 4.66 trillion rupees to absorb the shock, and paid for it with borrowing. Total public debt climbed to 83,285 billion rupees.

Today’s relief is being bought with tomorrow’s revenue.

Industry tells the same story from a different angle. Large-scale manufacturing grew 6.1 percent on cheaper credit, but Pakistani factories cannot expand without imported machinery and raw materials, so imports rose 6.9 percent and the goods trade deficit widened to 27.9 billion dollars. Each point of growth drains reserves, which reached 22.6 billion dollars by mid May 2026. Literacy stands at 63.0 percent, with men at 73.0 percent and women at 54.0 percent. Half the country’s talent remains locked out of the formal economy.

The sharpest shift is external.

The United Arab Emirates detained and deported over 15,000 Pakistani workers, then demanded immediate repayment of a 1 billion dollar loan. Saudi Arabia stepped in with a 3 billion dollar deposit and averted a payments crisis. This, in my opinion, is the most concerning trend, and the one worth watching.

Why did a fifty-year friendship turn punitive in a fortnight?

The UAE assessment

Let me run this by laying out the competing explanations rather than arguing a single one and hoping it sticks.

Three hypotheses explain the Baloch insurgency and the UAE’s posture toward it.

H1: the insurgency is indigenous, rooted in real Baloch grievances over resource extraction and disappearances, with foreign actors merely exploiting an opening they did not create.

H2: India is the primary external sponsor, with its documented historical role in Baloch networks, and the UAE serves at most as a financial conduit.

H3: UAE is the organizing hand behind the western pressure on Pakistan.

The useful judgment sits in the combination. The insurgency is indigenous in origin and increasingly useful to a set of external actors whose interests have converged. The question worth anyone’s attention is who now keeps it alive, and at what level of deliberateness. On that question, I assess with medium to high confidence that the UAE is a willing financial beneficiary, and that it actively directs BLA operations with the help of Afghanistan as the staging post and India as the enabler. The distinction matters for what Pakistan can do about it, and I return to that.

Now the case for why Abu Dhabi sits in the frame at all.

At the outset, the UAE read the 2025 Pakistan-Saudi defense pact as a defection, and read Islamabad’s neutrality toward Iran as betrayal. The deportations, the loan recall, and the canceled airport deal arrived too close together to be coincidence. Money owed, jobs held, and permits granted have all become instruments of pressure.

The story runs further back. The UAE accepted the credentials of an Afghan Taliban ambassador as early as August 2024, becoming only the second country after China to do so. MBZ met Sirajuddin Haqqani in January 2025 to discuss bilateral cooperation and reconstruction. UAE Foreign Minister Abdullah bin Zayed spoke by phone with Taliban Foreign Minister Amir Khan Muttaqi in March 2026, with the conversation focused on the Pakistan-Afghanistan conflict, after which Kabul pledged its soil would never be used against Islamabad. That call is publicly documented.

The fact that Abu Dhabi felt it necessary to make that call, and that it was about the Pakistan-Afghanistan conflict, tells you something. Whether it was asking the Taliban to hold back or asking them to moderate is genuinely ambiguous, and I will not pretend the call resolves either way.

The UAE has 3.5 billion dollars invested in Afghan infrastructure, including an aviation company close to Abu Dhabi’s national security adviser that was given access to Afghan airports. It maintains direct, high-level relationships with Haqqani Network figures. The Haqqani network used front companies and Afghan expatriates to recruit and launder money through the UAE for decades. United States pressure pushed those operations underground after 2014, but they continued. The Haqqani network is now the Taliban’s interior ministry. The UAE now holds formal bilateral relations with that ministry.

The UAE's behavior across multiple theatres follows a consistent pattern. It builds commercial and security penetration into fragile states: Sudan, Yemen, Somalia, Afghanistan. It uses that penetration to extract rents, whether gold, ports, or airspace. When a regional rival threatens Emirati interests, those commercial relationships become pressure instruments.

Consider the squeeze on Pakistan in full. Before demanding repayment, the UAE shortened historical 12-month rollover terms down to single months and more than doubled interest rates to 6.5 percent. Pakistan cleared the 3.5 billion dollar facility through a structured payment schedule finalized by April 28. State-linked enterprises moved in parallel:

Etihad Airways dismissed Pakistani personnel with as little as 48 hours’ notice.

Over 15,000 workers, mostly Shia Muslims, were detained and deported from Dubai since April, leaving behind luggage and savings.

NPR and Reuters detail thousands undergoing humiliating conditions in detention centers before forced removal.

Every move squeezed an already strained economy.

Why Gwadar is the organizing logic

Start with the economic fact, because the rest follows from it. Gwadar sits 87 kilometers from Iran’s border and close to the mouth of the Strait of Hormuz. Pakistani officials estimate it can contribute 18 to 25 billion dollars annually to Pakistan’s economy.

The port authority chairman has named the ambition outright: rival Jebel Ali.

That last point matters for everything after it. The Jebel Ali Free Zone alone hosts over 8,700 companies from more than 100 countries and contributes approximately 23 percent of Dubai’s gross domestic product. Dubai’s entire post-oil identity rests on being the indispensable logistics node between Asia, Africa, and Europe. Gwadar, fully operational, erodes that position for good. You cannot negotiate your way out of geography.

Economic analysts have described Gwadar as another Dubai emerging on the world’s map and frame the rivalry as a silent economic war in the Gulf of Oman, with Pakistan, China, and Qatar on one side, and India and the UAE on the other. The framing appears in Western economic literature and reflects a straightforward reading of competing port interests.

A state whose entire economic model depends on being the region’s indispensable logistics hub has a structural interest in ensuring the rival hub never functions. It needs no conscious decision to destabilize Balochistan. The interest exists whether or not anyone in Abu Dhabi has ever said those words aloud.

The ideological glue binding Israel, the UAE, and India is a shared view that political Islam threatens each government’s survival. Underneath the ideology sits hard convergence on one geographic problem: the China-Pakistan Economic Corridor and Gwadar.

For India, a fully operational Gwadar gives China a naval and commercial presence 400 kilometers from the Strait of Hormuz, bypassing Indian maritime chokepoints and cutting China’s energy shipping distance from West Asia from 13,000 kilometers to 3,000. India has spent decades trying to encircle Pakistan through Chabahar and outreach to Kabul because a stable, China-linked corridor through Balochistan would redraw the subcontinent’s balance for decades. The BLA targets Pakistan’s army and Chinese interests, including Gwadar itself.

For the UAE, the threat is commercial. DP World signed 3 billion dollars worth of agreements with India’s Gujarat state to develop ports and terminals, signed in the presence of MBZ and Prime Minister Modi. Abu Dhabi is building an alternative logistics architecture in the Indian Ocean, one that rests on Indian geography in place of Pakistani geography. If Gwadar works, that thesis weakens. If Balochistan stays volatile, Gwadar stagnates, and the Gujarat corridor becomes more attractive to every shipping line making routing decisions.

For Israel, a stable, prosperous Pakistan anchored to China and Saudi Arabia through CPEC and the mutual defense pact shifts the regional balance against it. A Pakistan consumed by internal security crises and squeezed economically cannot build the Islamic NATO bloc that Israel’s prime minister named as the threat requiring a Hexagon of Alliances counterweight, a proposal positioned against the Pakistan-Saudi-Turkey-Egypt grouping, with the UAE, Bahrain, and Jordan on the opposing side.

Three capitals. Three different logics. One geographic outcome they all gain from: Gwadar does not work.

The mechanism, and what it would take

Afghanistan under Taliban rule supplies the missing link. The UAE holds extensive financial and diplomatic ties to the Taliban regime. The Taliban regime provides, at minimum, passive sanctuary to the BLA, whose primary operational target is Gwadar. The UAE has a structural interest in Gwadar failing. And the UAE has a documented record, across Sudan, Yemen, and Somalia, of using financial relationships with armed non-state actors to pursue commercial objectives while keeping official deniability.

Understanding what the UAE does in Sudan makes the Balochistan inference more defensible, because the mechanism is identical.

The UAE imported 29 tonnes of gold directly from Sudan in 2024, up from 17 tonnes the prior year, with additional volumes routed through Chad, Libya, and Egypt, which analysts describe as exit points for RSF-controlled gold. Swissaid described these flows as confirming the UAE’s role as a major destination for smuggled conflict gold. The Sentry documented a 24 million dollar real estate portfolio in Dubai owned by family members and entities linked to RSF leadership, including sanctioned individuals.

The mechanism runs on financial infrastructure rather than direct weapons transfers, though those have been alleged. Dubai provides the laundering capacity, the legal residency, the banking access, and the commercial cover that lets a proxy sustain itself. The UAE issues no orders. It keeps the financial pipes open. The proxy finances itself and pursues its own objectives, which happen to align with Emirati interests.

Translate that to Balochistan. The requirement is financial networks in Dubai accessible to BLA leadership or their suppliers, combined with Afghan Taliban tolerance of BLA sanctuaries funded through those same networks. The UAE-Taliban financial relationship, now formalized through diplomatic recognition and banking cooperation agreements, creates exactly that infrastructure.

So the assessment holds at moderate to high confidence: the UAE is a willing beneficiary of the Baloch insurgency, a state whose financial networks let a proxy sustain itself without active direction. India’s role in BLA networks is better documented and more institutionally established, and that is what makes the chain workable. The partner with the operational history and the partner with the financial plumbing now sit on the same side of the ledger.

Whether Abu Dhabi has crossed from beneficiary to active facilitator is the question Pakistan’s establishment should press hardest, and the one open sources cannot answer.

What Abu Dhabi cannot do

The UAE is not an unconstrained actor.

Its post-oil model depends on the same Hormuz traffic Pakistan does. The Iran war showed Jebel Ali and Dubai International sitting inside missile range, soft targets whose disruption hit Emirati supply chains directly. The gold-laundering conduct described above put the UAE on the Financial Action Task Force grey list from 2022 to 2024, a reputational cost it worked hard to shed and would prefer not to revisit. And the coercion strategy carries a base-rate problem worth taking seriously.

Economic coercion designed to force a middle power to realign has a poor track record. The closest case is Qatar under the 2017 Gulf blockade, when the UAE and Saudi Arabia cut land, air, and sea links to force Doha into line. The result was the opposite of the intent. Qatar hardened, deepened its alignment with Turkey and Iran, and emerged more independent than before. The blockade collapsed in 2021 with none of its objectives met.

If that base rate applies, and coercion of this kind usually produces defiance rather than capitulation, then Abu Dhabi’s squeeze on Pakistan is more likely to push Islamabad further toward Riyadh, Ankara, and Beijing than to break the Saudi pact.

I assess with moderate confidence that the UAE’s pressure campaign hardens Pakistan’s alignment rather than reversing it. That does not make the campaign harmless.

A hardened, cornered, economically squeezed Pakistan is a more volatile neighbor, which may suit some of Abu Dhabi’s partners more than Abu Dhabi itself.

The three branches ahead

Over the next 90 days, the situation runs down one of three paths.

In the base case, which I put at roughly 55 percent, the ceasefire holds and the squeeze continues at current intensity. Pakistan absorbs the deportation and reserve pressure, leans harder on Saudi and Chinese buffers, and the Balochistan war grinds on without decisive escalation. Watch the monthly remittance figures. A second consecutive month of decline signals this branch is deepening.

In the downside, roughly 30 percent, the ceasefire breaks. Fuel and remittance shocks compound, inflation returns to double digits, and street unrest meets a security apparatus already at full stretch. The trigger to watch is the Washington-Tehran back channel. A collapse there precedes the economic damage by days, which is your warning window.

In the upside, roughly 15 percent, Tehran and Riyadh cool their rivalry, and Abu Dhabi’s substitution logic weakens because a calmer Gulf reduces the value of the India tilt. The signal here is any quiet UAE re-engagement with Islamabad, the kind of back-channel outreach that reverses a coercion campaign before it is publicly abandoned.

The recommendation that follows holds across all three branches, which is the point of naming them.

Emerging Signals

Coercion only works when the coercer has a substitute, and the UAE now has one. Abu Dhabi has spent two years building a partnership with India grounded in commercial pragmatism and shared hostility to political Islamic movements. The Emirati leadership scrapped the Islamabad airport project soon after a state visit to New Delhi. It finances the Rapid Support Forces in Sudan and pursues territorial control in Yemen. Once a partner becomes replaceable, the old interdependence turns into a handle for pressure rather than a cushion against it.

Pakistan is responding by selling the one asset it still owns in abundance: position.

Islamabad delivered direct United States and Iran talks on April 11 and 12, the highest level contact since 1979. The military leadership then converted diplomatic standing into cash. A United States metals company signed a 500 million dollar mining agreement with the military, a sign that Islamabad now courts transactional, resource based western investment to replace fading Gulf patronage.

The logic is cold and clear. If old friends will not fund you on loyalty, new partners might pay you for usefulness.

What This Means

For investors, the transmission channel that matters is remittances, which feed the current account and the rupee. UAE-sourced remittances were running near 824 million dollars a month before the deportations. A sustained drop pressures the currency and, by extension, the energy and import-heavy names on the KSE-100. A Hormuz closure is the tail risk that hits hardest: it spikes fuel costs, widens the import bill, and compresses margins across the listed industrial base at the same moment reserves are thin. If you think the bloc realignment is mispriced and Pakistan hardens toward China and Saudi rather than breaking, the asymmetric position is in assets exposed to a Saudi and Chinese capital backstop rather than Gulf-wide sentiment. Size it small and treat the ceasefire back channel as your stop loss. None of this is investment advice, and you should verify every figure against primary data before acting.

For businesses, the exposure is supply chain and contract terms. Firms routing through Jebel Ali or dependent on UAE-based logistics now carry a political risk that did not exist a year ago, since the same state that handles your freight has shown it will weaponize commercial relationships against Pakistani interests. The hedge is redundancy: a second routing option, even at higher cost, and contract language that does not assume Gulf goodwill. Anyone with Pakistani labor exposed to UAE residency rules should treat that workforce as suddenly fragile.

For the public sector, the lever is sequencing, and the order is the whole game. Reserve adequacy comes first, because the April episode showed a friendly facility can become a margin call overnight. Labor diversification comes second, with eyes open about its limits, which I set out below. A discreet predictability channel with Abu Dhabi comes third, aimed at lowering the cost of the next crisis rather than at reconciliation that is not on offer.

Citizens absorb the shock first.

Strikes on Qatari infrastructure disrupted liquefied petroleum gas supplies, so families face prolonged power outages in the hottest months. Renewed Gulf fighting would push transport and food costs through household budgets that have no cushion left at 28.9 percent poverty.

The one bright patch is digital.

Information technology generated a trade surplus of 2.91 billion dollars and telecommunications contributed 285 billion rupees to the exchequer, a path the government can keep open only by resisting the urge to over tax it.

A closing note on concentration risk.

The state registered 762,499 workers for overseas jobs in 2025, and remittances reached 30.3 billion dollars from July to March. The Emirati deportations targeted specific communities, turning identity into a tool of punishment for Islamabad’s neutrality. A country that earns its foreign exchange from one region has handed that region a veto over its foreign policy. The survey names 2025 the second warmest year in 65 years, so climate shocks will compound every fragility above.

What To Watch Out For In The Coming Week

Watch the finance bill debates, where opposition parties plan sustained protest inside the National Assembly. Track the withdrawal of tax exemptions for the former Federally Administered Tribal Areas, which risks inflaming a volatile region. Observe the western border, where the military claims 415 insurgents eliminated in Operation Ghazab lil-Haq. Follow the Washington and Tehran back channel, since any ceasefire breakdown hits Pakistani fuel prices within days. Watch for sudden regulatory moves on foreign direct investment.

Takeaways

Separate survival from any single relationship, but cost the separation honestly.

Pakistan needs to substantiate the role UAE is playing in its destabilization, and reduce its reliance on the state for labor exports. Formalizing labor corridors with East Asia and East Africa is the standard advice, and on its own it is close to useless in the near term. East Africa cannot absorb a meaningful share of two million Gulf-based Pakistani workers on any horizon under five years, and the wage differential is a fraction of what the Gulf pays, so remittance value per worker falls even where placement succeeds. The realistic near-term move is defensive: a contingency fund sized to a sudden remittance drop, a diplomatic floor under the remaining Gulf relationships, and diversification treated as a decade-long build rather than a crisis fix.

Second, in order to enhance the state’s role as the regional stabilizer, policy makers need to replace bilateral loans, which carry political conditions, with multilateral buffers, which do not. Build a credible tax on agricultural income and retail, because squeezing the documented sector yields revenue today and stagnation tomorrow. Keep the United States and Iran dialogue alive without alienating Riyadh or igniting sectarian anger at home.

Then test every assumption before events do. Under present conditions, there is no room for surprise.

The state is on two ropes at once, fiscal and geopolitical, and this week it has shown the world it can walk the second one. The first rope is the one it has never learned to cross. A country that owes 51 paisa of every rupee before it governs cannot fund the security that would close the Gwadar question, and the actors who gain from that question staying open are betting it never will. Diplomatic audacity bought Pakistan one extraordinary season. Only fiscal discipline buys it five years. The re-rating waits on the second rope, not the first.

— Syed Ali Shehryar