Weekly Brief | Week of February 23, 2026

Pakistan’s risk tilts from “managed stress” to “corridor squeeze” as Iran war and Afghan line heat up

War Pressure On Both Flanks

Pakistan is watching live US and Israeli missiles hit Iran while actively fighting militant Afghanistan. It has moved from warning Kabul to bombing targets in Kabul, Nangarhar, Khost, and Paktika within days of fresh attacks at home. For leaders with exposure to Pakistan, the question is “How far can a state fighting a live border war, under an Iran conflict and IMF rules, still honour contracts and keep macro gains.” The core problem this week is how war on two western arcs and oil risk reshape Pakistan’s corridors, not whether Pakistan is willing to hit back.

This Week In Brief

Pakistan has carried out intelligence led airstrikes against seven camps in Nangarhar, Paktika, and Khost, then widened fire under Operation Ghazab Lil Haqq after a month of suicide attacks in Islamabad, Bajaur, and Bannu. Kabul calls this a breach of its territory; Islamabad calls it overdue punishment for TTP and allied groups that plan from Afghan soil. At the same time, the United States and Israel have hit Iranian command and missile sites, Iran has replied with drones and missiles, and Iran backed Houthis have again threatened Red Sea routes, lifting oil by about 3 to 4 percent and pushing 2026 price forecasts higher.

FX reserves at the State Bank are about US$16.2 billion, total liquid reserves are above 21 billion, January CPI is 5.8 percent inside the 5 to 7 percent target band, and Islamabad is on course for the next IMF review. That cuts short horizon default and pure FX crisis risk into the “unlikely” band. The big swing is elsewhere: regional war and oil pressure now sit around 60 to 70 percent (likely to very likely), and the Afghanistan–Pakistan clash has moved from sporadic fire to open war with stated intent to “eliminate” TTP leadership wherever found. India has not shifted posture this week, so a hot eastern front remains very unlikely, but a probe in a stressed moment would carry high cost if it came.

Governing Thought And Posture

Pakistan is in a 12 month stretch of medium risk driven by three things: regional war and oil, AfPak conflict, and the need to stay inside IMF lines while fighting live enemies. Regional war and oil stress is now roughly 60 to 75 percent (likely to very likely) after strikes on Iran, new Red Sea threats, and higher 2026 oil projections. Cross border security risk sits in the same band after 699 attacks in 2025, a demarche over Bajaur, and now cross border strikes and Operation Ghazab Lil Haqq. Short horizon default risk has dropped to roughly 25 to 35 percent after IMF board approvals and steady reserve gains.

This shifts risk from “will Pakistan pay?” to “which corridors and sectors still make sense under war, oil, and coercive strikes.”

Pakistan is investable this week only on a selective and hedged basis: the state has shown it will hit back hard westwards, but that same fight plus Iran war and shipping stress tighten every corridor.

This Week’s Risk Shifts

Regional war and oil linked external stress – ⬆️

Prior: 45–55 percent (even chance)

New evidence: US and Israeli strikes on Iran’s leadership and missile infrastructure, Iran’s drone and missile reply across the region, and Iran backed Houthi threats have pushed oil up by about 3–4 percent and lifted 2026 price forecasts by nearly 2 dollars a barrel.

Updated: 60–75 percent (likely to very likely).

Impact: Higher fuel and freight bills, rougher current account math, and more pressure for tariff hikes at home.

Afghanistan–Pakistan conflict – ⬆️

Prior: 45–55 percent (even chance) that clashes would stay at low burn.

New evidence: Pakistan has issued a demarche over Bajaur, then carried out intelligence based airstrikes against seven TTP and ISKP camps in Nangarhar and Paktika, and then widened fire and ground moves under Operation Ghazab Lil Haqq; Afghan forces have replied, and both sides speak of war and large enemy losses.

Updated: 60–70 percent (likely) that fighting stays live over the next year.

Impact: Higher security spend, more risk premium, and slower timelines for assets and routes in KP, merged districts, and Balochistan.

Two front scare with India layered on west – ↗️(slightly up)

Prior: 10–20 percent (very unlikely).

New evidence: No new Indian build up or clash this week, but Pakistan is now in open fighting on the western front while Iran war pulls in US and Gulf assets, which reduces slack in the system.

Updated: 20–30 percent (still unlikely).

Impact: Even a short India scare on top of this would hit PSX harder than the recent US–Iran moves, widen spreads, and could force FX and trade steps that undo IMF gains. This remains a scenario, not a base.

Near term default and pure FX crisis – ⬇️

Prior: 55–65 percent (likely) during the 2022–23 crunch.

New evidence: IMF board cleared the second review and released 1.2 billion dollars; staff and local work show Pakistan broadly on track, and SBP reserves now stand near 16.2 billion dollars with total liquid reserves over 21 billion and targets above 17 billion by mid 2026.

Updated: 25–35 percent (unlikely).

Impact: Lower odds of outright payment stop in the next year even under war and oil stress.

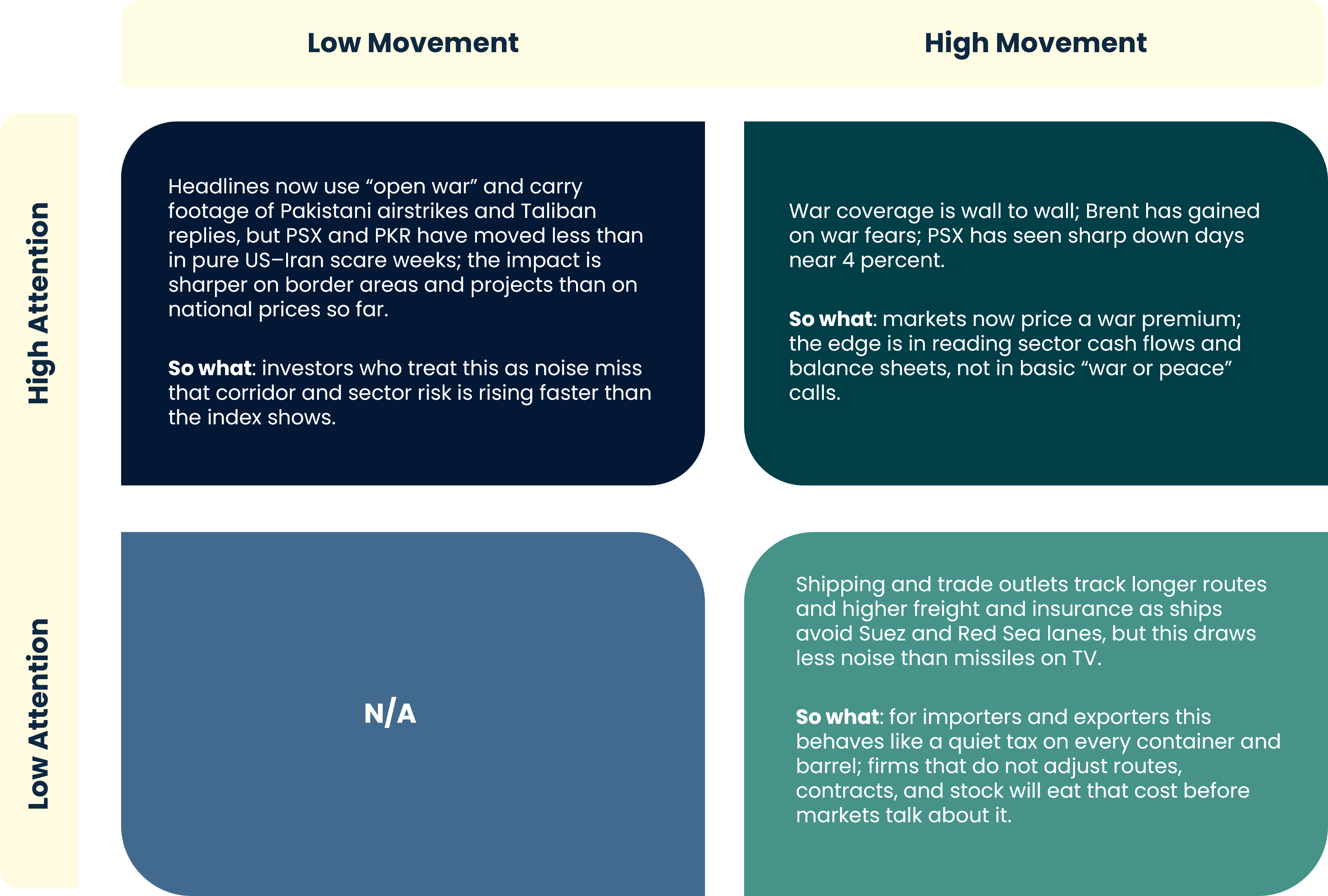

What’s Moving, What’s Not (Attention vs Movement)

In this matrix, “attention” is media and commentary; “movement” is prices and real flows. Attention is high when an issue dominates major outlets, low when only a narrow crowd watches it. Movement is high when prices or real indicators shift by more than about 2 percent; low when they barely move.

Outside Pakistan: Global And Regional Moves

Global rates remain high, while Iran war adds a fresh layer of oil and risk premia. For Pakistan this pulls on the current account, budget, and IMF path by raising the fuel bill just as the state tries to clean up power sector arrears and hold inflation near 5–7 percent.

Red Sea raids and threats have cut traffic and pushed ships around Africa, adding days and cost to voyages to and from Europe. Pakistan’s exporters and importers who use these routes face higher freight and insurance; if firms and state bodies do not adjust, that cost shows up as thinner margins or higher prices.

Afghanistan–Pakistan now sits as a live regional flashpoint: Kabul gives cover and space to TTP and tells Pakistan to solve TTP “internally”, while Pakistan actively engages, foregoing the previous passive stance, the Durand Line and declares its patience over. India has stayed outside this fight so far, but closer Kabul–Delhi links and Afghan use of Indian equipment keep Delhi in the background of Islamabad’s calculus.

Inside Pakistan: Politics, Macro, Policy, Society

On the geopolitical side, Pakistan has moved from demarches and warnings to sustained cross border force, active protection of its sovereignty, and has the evidence of Afghan Taliban being partners of TTP and as part of a hostile network that also uses India backed proxies. This hardens public support for action in the west and signals that Islamabad will no longer treat Afghan soil as off limits when TTP kills its soldiers and citizens.

Domestic politics remain under strain from years of unrest, legal fights, and elite rifts, but there is no fresh collapse or new development this week. War pressure can both rally support and deepen mistrust, depending on how losses and costs are shared.

Macro numbers are better than in 2022–23: reserves are above US$16 billion at SBP, total liquid above US$21 billion; CPI is 5.8 percent; SBP and IMF see growth picking up if oil and security stay within bands. War and oil now test that story.

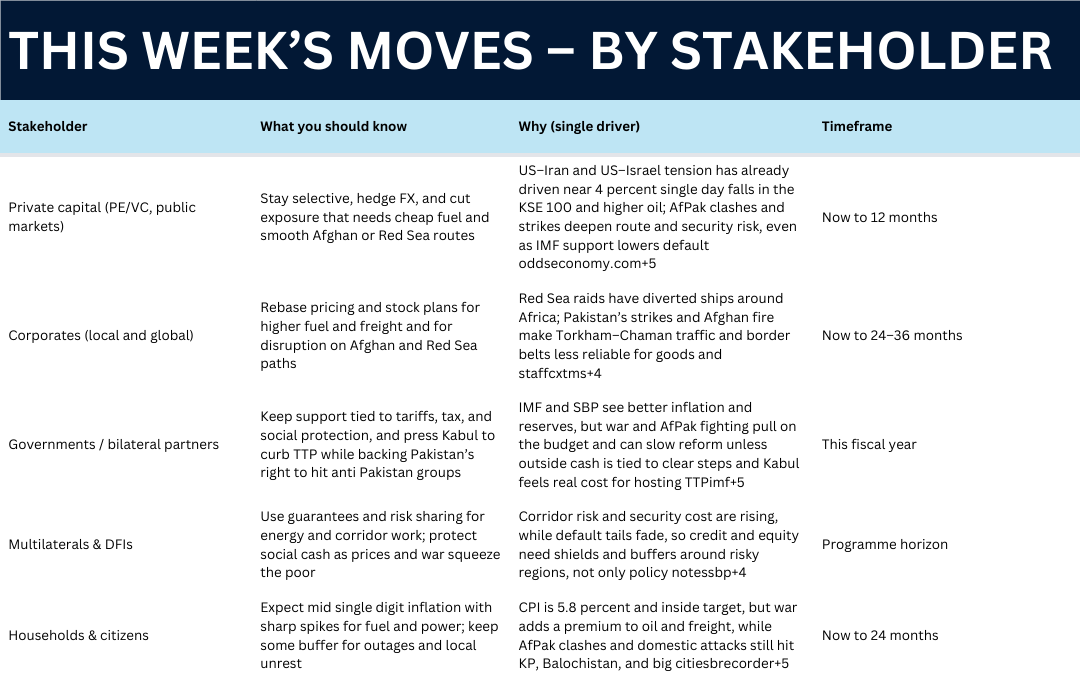

What This Means For You

For private investors, the main risk now runs through energy, freight, and corridor security rather than pure default. Time to be cautious on assets that need smooth Afghan trade, border access, or cheap regulated fuel.

For public markets, US–Iran tension and AfPak war have already produced some of the steepest KSE 100 swings of the past year. We’ll see FX hedges; bond duration kept short to medium; an equity tilt toward banks, exporters, and firms with pass through of fuel and freight.

For governments and IFIs, the question is how to keep pressure on tariffs and tax while Pakistan fights real enemies and shields the poorest from war and price shocks. The administration will need to link cash to concrete steps on energy and tax; build in more support for social cash and border zones; work channels with Kabul and Doha to curb TTP without asking Pakistan to “absorb” endless fire.

For corporates, supply chains that rest on one port, one sea lane, or one border crossing now carry extra risk, and fuel touches every line of cost. It is time to diversify routes and ports; add stock of key imports; change contracts to share fuel and freight risk; update plans for air space closure, target attacks on depots, and strikes on telecom links.

For households, the mix of war, oil, and domestic politics means mid single digit inflation with spikes on fuel, power, and some food, plus some risk of outages and unrest in KP, Balochistan, and big cities.

What To Watch Next Week

Three tracks will tell you most about how Pakistan’s state handles a real two front squeeze: the next IMF review, the course of Operation Ghazab Lil Haqq and Afghan replies, and energy pricing under war.

If Islamabad clears the next IMF review on time and still raises tariffs in line with the plan, markets will see that even in war the state can keep its macro word. If AfPak fighting widens or Kabul strikes deep inside Pakistan, corridor and project risk will jump again and call for a tougher stance from partners toward Kabul. If oil stays high and tariffs stall, circular debt and hidden bank risk will grow back.

The pattern this week is clear. Moves that ride on external anchors and narrow teams, like IMF reviews and cross border strikes, still happen. Moves that need broad cover at home under high prices, like deep energy and tax changes, slow down.

Interesting next few days. Until then, let’s pray for peace and better times.