Weekly Brief | Week of February 16, 2026

Power tariff re-pricing and security shocks are tightening Pakistan’s decision space

For: PE/VC [✓] | Public Markets [✓] | Corporates [✓] | Govts/IFIs [✓]

Pakistan is simultaneously over-governed and under-governed, and investors feel both. For leaders with exposure to Pakistan, the hard part this week is not spotting noise in headlines, but judging how much room the state really has on funding, security, and digital control before something breaks. The core problem is simple to state and hard to price: can Pakistan sustain a narrow path of “managed stress” without tipping into another balance-of-payments scare or political shock. The weekly brief covers this, through my lens and based on the signals I found worth tracking for the week. It’s something new I am trying and you will see it expand, improve and cover more dimensions in the future iterations. I’ll wait for your feedback!

This week in one page

Stabilization’s Split Screen

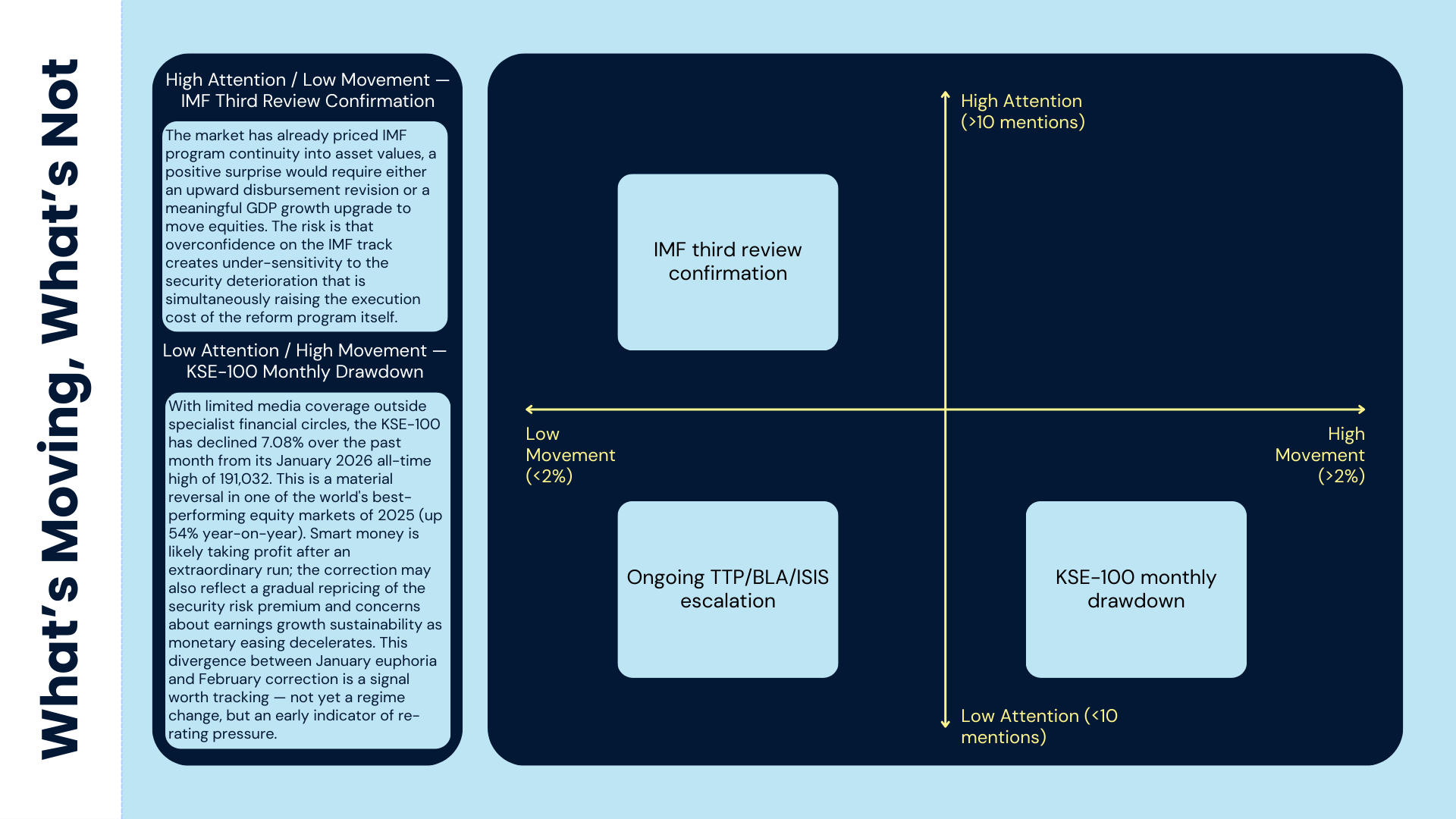

IMF momentum holds as security deterioration widens the execution gap

This week, our focus was on the structural divergence between Pakistan's IMF-tracked macro stabilization and its rapidly deteriorating security environment as the twin drivers of risk and opportunity for every stakeholder with Pakistan exposure.

Pakistan is in a period of constrained stability where formal default risk looks lower than in 2022–23, but external funding, domestic politics, and security still sit near the edge of what markets will accept. FX reserves have improved from the worst of the crisis but remain thin for an import-dependent country, which means any oil spike, delay in official inflows, or surge in outflows can still reopen the stress channel fast. Inflation has eased from its peak yet stays high enough to hurt real incomes and keep pressure on the central bank, while growth remains weak, so the sense of “macro normalisation” feels fragile rather than secure.

For investors and firms, the main shift relative to the previous crisis phase is in the shape of risk, not its level. Short-horizon default or convertibility fear has eased, but medium-horizon worries about execution of tax and energy reform, delivery on privatization, and the durability of the current political settlement matter more. The state has bought time; it has not bought much room to reverse course on tough measures without reopening IMF and market concerns.

Risk posture for Pakistan

A reasonable base case for early 2026 is that Pakistan remains investable on a selective and hedged basis, with country risk still priced above many frontier peers but not at outright distressed levels. That means capital allocators have to decide where controlled exposure still pays, rather than whether to exit the country entirely. In simple terms, the dominant constraint is external balance pressure, with political and security constraints sitting just behind it.

Funding risk now behaves less like a single cliff event and more like a series of rolling tests. Each IMF review, each large Eurobond or bilateral repayment, and each budget cycle tests whether Islamabad can keep delivering unpopular measures on taxes, energy tariffs, and SOE reform without triggering broad unrest or a breakdown in the coalition. If those measures stall, the next test is rarely far away: rating agencies, local yields, and the currency tend to move well before official default comes into view. Nonetheless, IMF confirmed its third review mission from February 25 to conduct discussions on the third EFF review and second RSF review. The IMF publicly stated that Pakistan’s reform implementation has helped “stabilise the economy, rebuild confidence,” and described fiscal performance as “strong” with headline inflation “relatively contained”. FX reserves stand at $16.197 billion at SBP and $21.3 billion total. CPI inflation at 5.8% in January 2026 remains within SBP’s 5–7% target range. PKR steady at 279.52 per USD. Primary surplus tracking at 1.3% of GDP.

Second order effects matter more than before. If the government leans too hard on energy and tax hikes to meet fiscal targets, it squeezes households and small firms, which then raises the risk of protests and weakens the political mandate for reform. That in turn makes reform delivery slower and noisier, which pushes up the risk premium on new funding, feeding back into the original fiscal problem. The “game” for investors is no longer to guess whether Pakistan will reform, but to judge how much reform can pass before politics and security push back.

What’s Moving, What’s Not

For those new here: Attention measures media coverage intensity, with High being more than 10 media mentions. Movement captures observable market or operational impact, with High being more than 2%. Mismatches between attention and movement often signal mispricing or early trends worth tracking.

What moved outside Pakistan

The external backdrop for Pakistan remains tight. Global rates are off their peak but stay high enough that marginal EM borrowers pay a steep price for market access, and Pakistan is still in the group where new hard-currency issuance competes poorly with concessional and bilateral flows. That keeps the country dependent on IMF support, Gulf partners, and Chinese rollovers, and it raises the bar on any move that would alarm those creditors, such as loose fiscal policy or erratic FX management.

Energy and regional security link back into this. Any firm upward move in oil prices quickly reopens the import bill channel and strains the current account, especially if growth recovers even modestly and pulls in more imports. Tension across the Gulf, in the Red Sea, or around Iran increases not only headline risk but also shipping costs and insurance premia, which show up in Pakistan’s trade bill and can bleed into domestic fuel and food prices. Border security issues with Afghanistan, or renewed friction with India, raise the prospect of higher security spending and deter some types of FDI, especially in exposed regions.

In totality, the chain runs through financing conditions. If global risk appetite worsens or sanctions and compliance rules tighten around any of Pakistan’s main partners, those partners may offer less generous rollovers or demand stricter conditions. That then narrows Islamabad’s room to slow reforms ahead of elections or in response to protests, and raises the chance of abrupt policy moves that unsettle investors.

What moved inside Pakistan

Domestic politics in early 2026 still revolve around a hybrid system cooperating and working in tandem for reforms to progress. Coalition management, court decisions on election-related cases, and informal civil–military understandings combine to shape the “band” in which policy can move. That band is not wide. Any perception of mass disenchantment, especially around prices, jobs, or perceived unfairness in accountability, quickly hardens the political constraint and slows structural measures.

On macro policy, the core story remains familiar. Fiscal consolidation relies on higher energy tariffs, broader tax effort, and some restraint on provincial and federal spending. Each move has direct distributional effects: higher power and fuel prices push up costs for industry and households; stricter tax collection meets resistance from trade and professional lobbies; cuts in development spending hurt patronage networks that politicians rely on. When this resistance rises, the temptation grows to protect some groups with exemptions or delays, which then weakens the fiscal path underpinning the IMF programme and market confidence.

Security risk is no longer a pure frontier issue confined to borderlands. Attacks in Khyber Pakhtunkhwa and Balochistan, pressure on Chinese-linked projects, and sporadic urban incidents all affect investor sentiment and the cost of doing business. Even if headline casualty numbers stay below past peaks, the perception that Western or Chinese personnel are at higher risk feeds through into higher security costs, tougher insurance, and more demanding terms from foreign sponsors. Over time, this can tilt the project mix toward those backed by states willing to absorb higher security costs, reducing the space for purely commercial deals.

Digital and information controls add another layer. Moves toward tighter content regulation, possible firewalls, or data localization rules may feel manageable from a domestic political angle, yet they raise reliability and compliance concerns for IT and BPO clients abroad. The first order effect is higher operational friction for exporters. The second and third order effects are more subtle: some clients may quietly diversify away, local firms may find their valuations discounted because of perceived “regulatory outage risk,” and the country’s narrative as a services exporter may erode even without a single headline ban.

Implications for decision makers and investors

For PE and VC funds, the main risk channel has shifted from sudden macro collapse to exit and convertibility risk over a 5–7 year horizon. Local-currency returns can still be attractive in selected consumer, export, and infrastructure-adjacent plays, but sponsors need to assume chunky FX moves at exit and consider partial natural hedges through USD or GCC revenue links where business models allow. The biggest error now is not entering Pakistan at all, but misjudging which sectors and partners can operate under a regime of tight FX, high energy costs, and intermittent regulatory jolts.

Public markets investors face a different balance. Sovereign and quasi-sovereign paper rewards careful duration and FX management more than heroic yield-chasing, with scope to earn carry when IMF and bilateral flows are on track but with sharp drawdown risk around any hint of programme slippage or security shock. Equity investors need to separate firms that can pass on higher energy and tax costs and access FX for inputs from those that sit at the mercy of controlled prices or import restrictions. In both credit and equity, state actions around SOE reform and privatisation will continue to create episodic entry points, but execution risk and political timelines matter more than headline plans.

For corporates already in Pakistan, the task is to rebase operating models for a world of higher energy tariffs, more assertive tax enforcement, and possible digital constraints. That means revisiting pricing power, supply-chain resilience, and local vs imported input mixes, along with hard-headed continuity planning for connectivity, security, and logistics. Foreign firms that treat Pakistan as a marginal market with thin management attention will struggle; those that treat it as a testbed for operating under constraint can still earn healthy returns.

Governments and multilaterals have to weigh their own constraints. Donors and IFIs want credible reform and social stability at the same time. Too much pressure on tax and tariff measures without support for social protection and service delivery risks fuelling unrest and weakening reform coalitions. Too little pressure risks another drift into arrears and under-collection. The most useful contribution now is less about new flagship loans and more about tightening the links between disbursements, delivery on core reforms, and shielded support for the poorest.

What to watch next

Three reform tracks offer the cleanest read on state capacity over the next few quarters. First, energy pricing and circular debt: whether Islamabad can keep raising tariffs and cleaning up collections without resorting to blanket subsidies again when protests bite. Second, tax and documentation: whether the authorities can broaden the base into under-taxed sectors rather than leaning again on already compliant segments. Third, SOE reform and privatisation: whether deals in power, aviation, and other core sectors actually close, not just move through cabinet approvals.

The second and third order questions follow from each track. If energy reform stalls, arrears will climb again, banks’ exposure to the power sector will deepen, and fiscal space for social spending and security will narrow, which then raises both social and security risk. If tax reform remains narrow, the state will keep “taxing inflation” through energy and indirect taxes, which further erodes trust and fuels informalisation, reducing the base in future. If SOE reform fails, private capital will demand higher returns or walk away, leaving more of the burden on already stretched public banks and external partners.

Over time, a pattern is likely to stand out. Actions that need deep political cover and long execution chains, such as across-the-board tax documentation, will move slowly or stall. Measures that can be pushed through executive orders and small teams, such as targeted digital controls or selective tariff tweaks, will move faster. For investors, that means technical reform design matters less than the ability to read constraints early, structure deals around them, and move fast when narrow execution windows open.

Closing: capability, not just calls

Why do smart funds still misprice South Asia risk? In Pakistan’s case, the answer now lies less in misreading the odds of any single event and more in underestimating how narrow the operating band has become for the state and for firms. Leaders with exposure here need to assume that tight funding, patchy security, and intrusive regulation are the baseline, not an exception that will fade.

Guessing the exact date of the next IMF review or court ruling is no longer the edge. The edge lies in building a repeatable way to read how Pakistan’s constraints move from week to week and quarter to quarter, and then wiring that reading into capital allocation, operations, and risk controls. Teams that do this tend to make two better moves: they cut avoidable damage earlier when the evidence turns, and they see where future revenue, influence, and supply security can still grow even as the map shifts around them.

This week, three questions are worth an hour of serious work.

Which single fault line would hurt us most if it moved faster than we expect: FX, security, or digital control?

Where are we still assuming Pakistan “calms down” within a year, despite the evidence of tight constraints across funding, politics, and security?

What is one decision we can pre-commit now, with a clear trigger such as an oil spike, border closure, or FX band break, so we are not improvising under stress?

The tension that opened this brief still holds. Pakistan is over-governed in rules and under-governed in delivery, and investors feel both. Those who accept that this environment will not soften on the timeline most plans assume, and who build the skills, systems, and judgement to turn Pakistan’s noise into a steady signal, are the ones most likely to still be writing cheques and building here when others have cycled out.