Weekly Brief | Week of April 3, 2026

Pakistan's fiscal bleed goes (very, very) public with an unprecedented petrol hike and economic indicators ringing all sorts of alarm bells

Summary

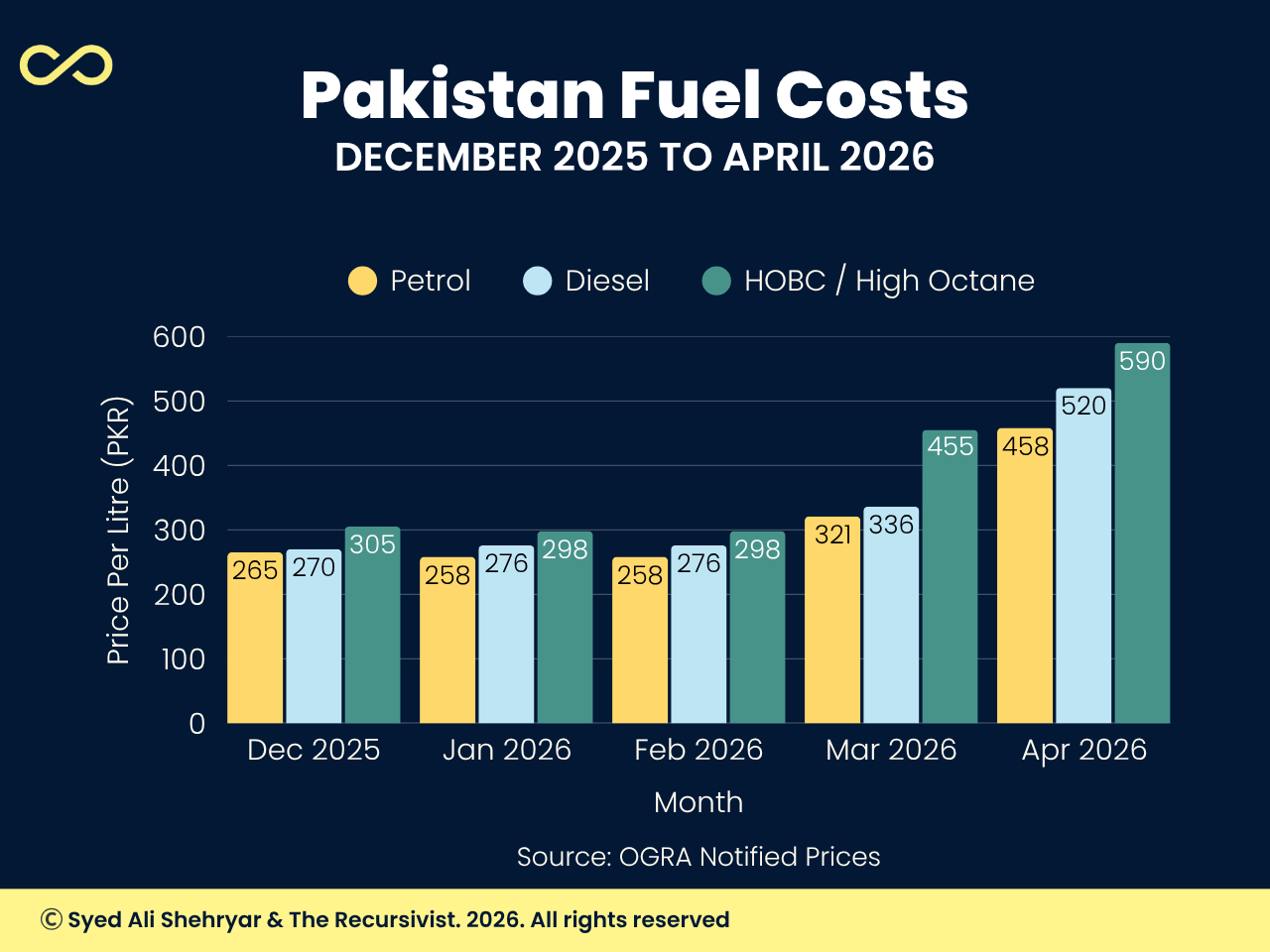

At midnight on April 2, a government notification raised petrol by Rs137 per litre, taking the pump price to Rs458.40.

Seventy million Pakistanis already live below the poverty line, real wages have not moved in three years, and FBR (the Federal Board of Revenue, Pakistan’s main tax collection body) is Rs610 billion short of its nine-month target with no credible plan to recover before June.

The government had no fiscal room to absorb any of the Gulf oil shock, so it passed the entire cost to consumers.

For the next 30 to 90 days, expect elevated inflation, falling household spending, growing political pressure, and a probable third downward revision of the FBR target, all while Pakistan runs an active military operation on its western border.

Pakistan’s relationships with Gulf states and China are currently providing the financing bridges keeping the economy afloat. Both depend on Pakistan appearing stable, and this hike is now putting that stability under direct pressure.

What Changed

The Price Shock and What It Reveals

Triggered externally and by internal mismanagement, Petrol rose Rs55 on March 7 and Rs137 on April 2 — a 43% cumulative jump in four weeks.

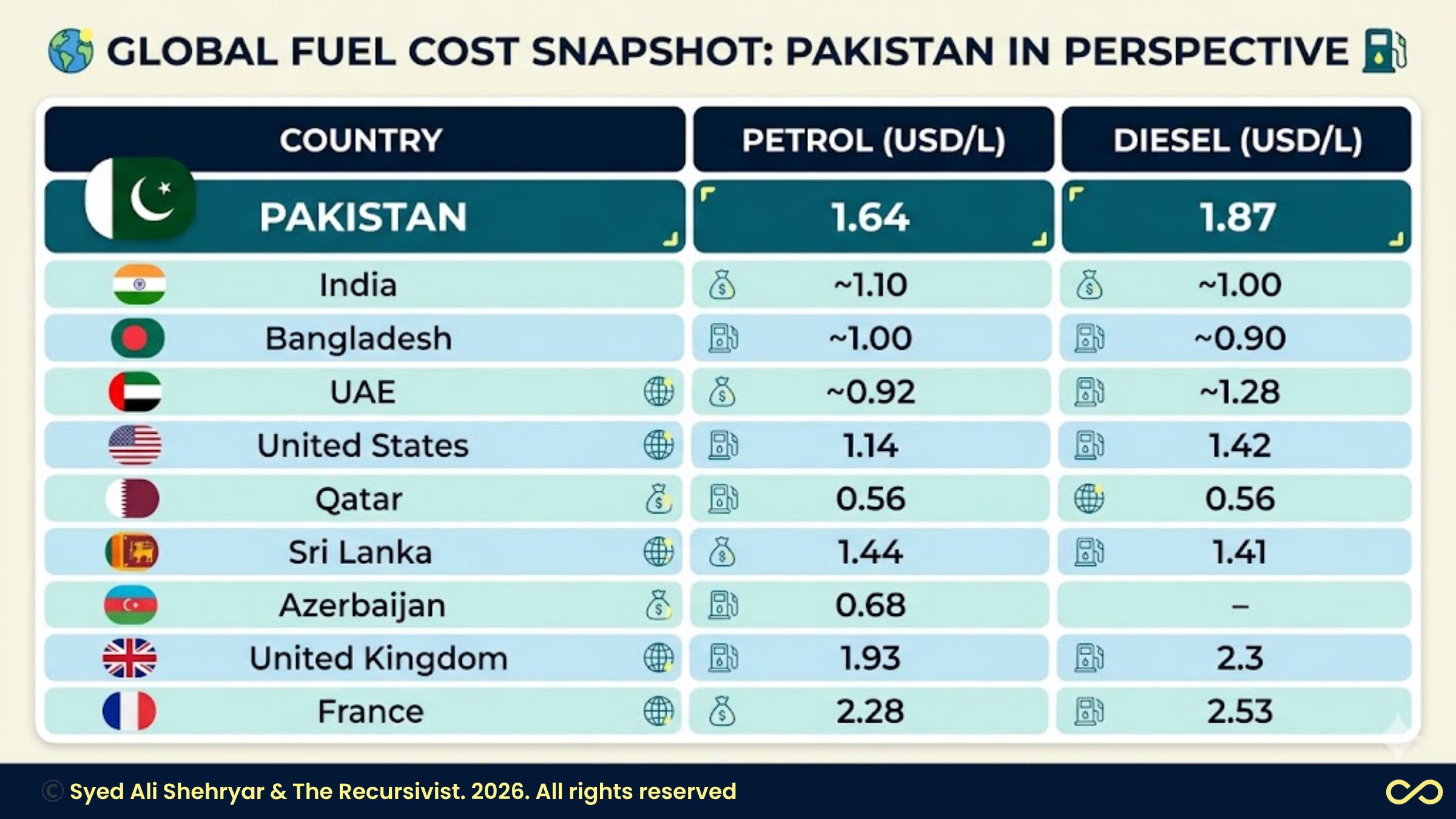

Oil prices jumped 20% in early March on Iran war fears, and Pakistan was identified as one of the most exposed economies in the world. But the reason every rupee of that shock landed on the consumer, rather than being absorbed by any government buffer, is a domestic failure.

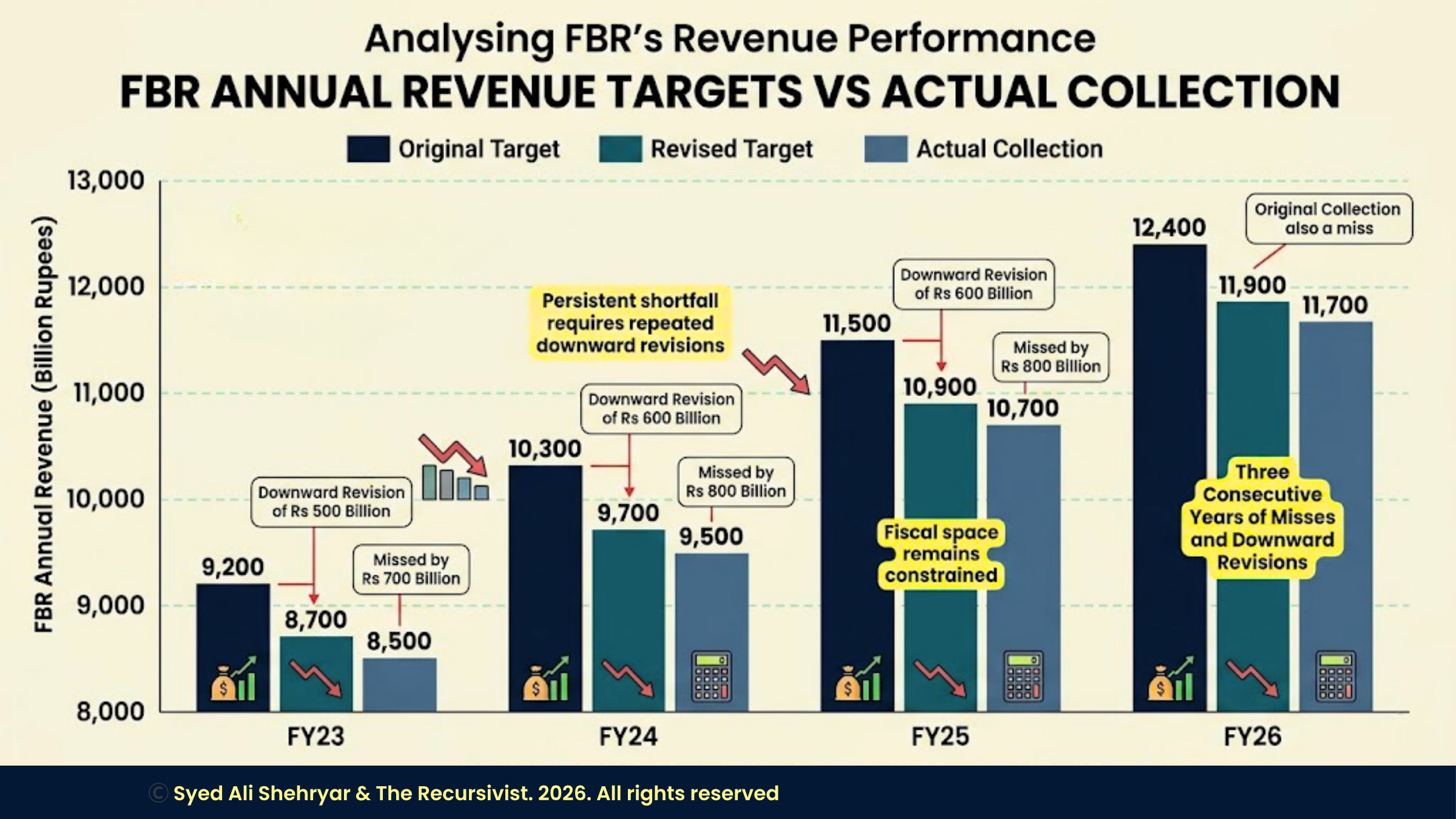

FBR collected Rs9.307 trillion against a target of Rs9.917 trillion in the first nine months of FY26, leaving a Rs610 billion hole. March alone added Rs182 billion to that gap through three simultaneous hits:

Import tax receipts fell Rs64 billion as Gulf war disruptions reduced trade volumes,

LNG shortages shut fertiliser plants and cost Rs40 billion in lost revenue,

Refunds issued by FBR nearly doubled, rising to Rs61 billion from Rs34 billion the month before.

The government’s response was to raise the petroleum levy, a charge that sits outside FBR’s books and does not count toward the official tax-to-GDP ratio.

With that, it has moved to cut development spending to give an artificial sense of fiscal stability.

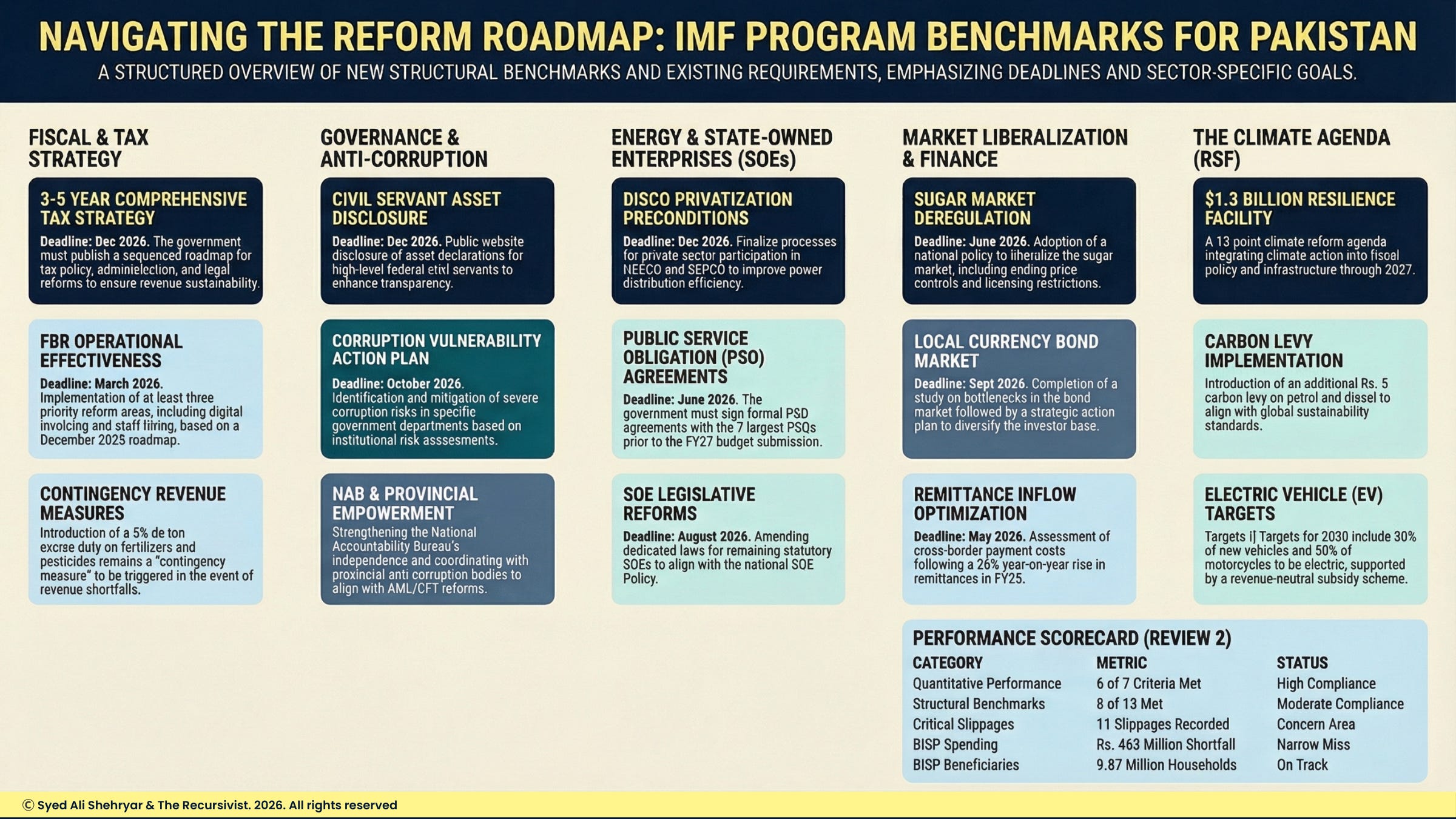

FBR now needs Rs4.672 trillion in the remaining three months of FY26 to meet even the already-lowered target. No official or analyst has made a credible case that this is achievable.

The Structural Problem the Shock Exposed

The FBR gap did not start with the Iran war. FBR missed its FY25 target by Rs178 billion after two downward revisions, and the Tajir Dost Scheme (a government programme to bring traders into the tax net) raised near-zero revenue against a Rs50 billion target.

Pakistan is now negotiating its second downward revision of the FY26 target, from Rs13.979 trillion to Rs13.45 trillion, which would still deliver only 10.6% in tax as a share of GDP against the agreed 11%.

Miss, revise down, miss again. Three fiscal years in a row.

A research paper published by FBR’s own staff names the structural cause directly:

Placing a non-professional generalist in the FBR Chairman role is the most important variable behind Pakistan’s chronically low revenue performance, with Pakistan’s tax collection described as “among the lowest in the world.”

The Finance Ministry runs on a similar pattern:

Staffed mainly by rotational civil servants moved between posts every few years, rather than by economists and revenue specialists who build expertise over time.

Each external shock therefore finds the same unfixed revenue base that IMF tries to fix. Not the cabinet. Not parliament. That is where Pakistan sits in the arc of a state in financial trouble: The decisions that matter most are made outside its own institutions.

The Social and Security Context

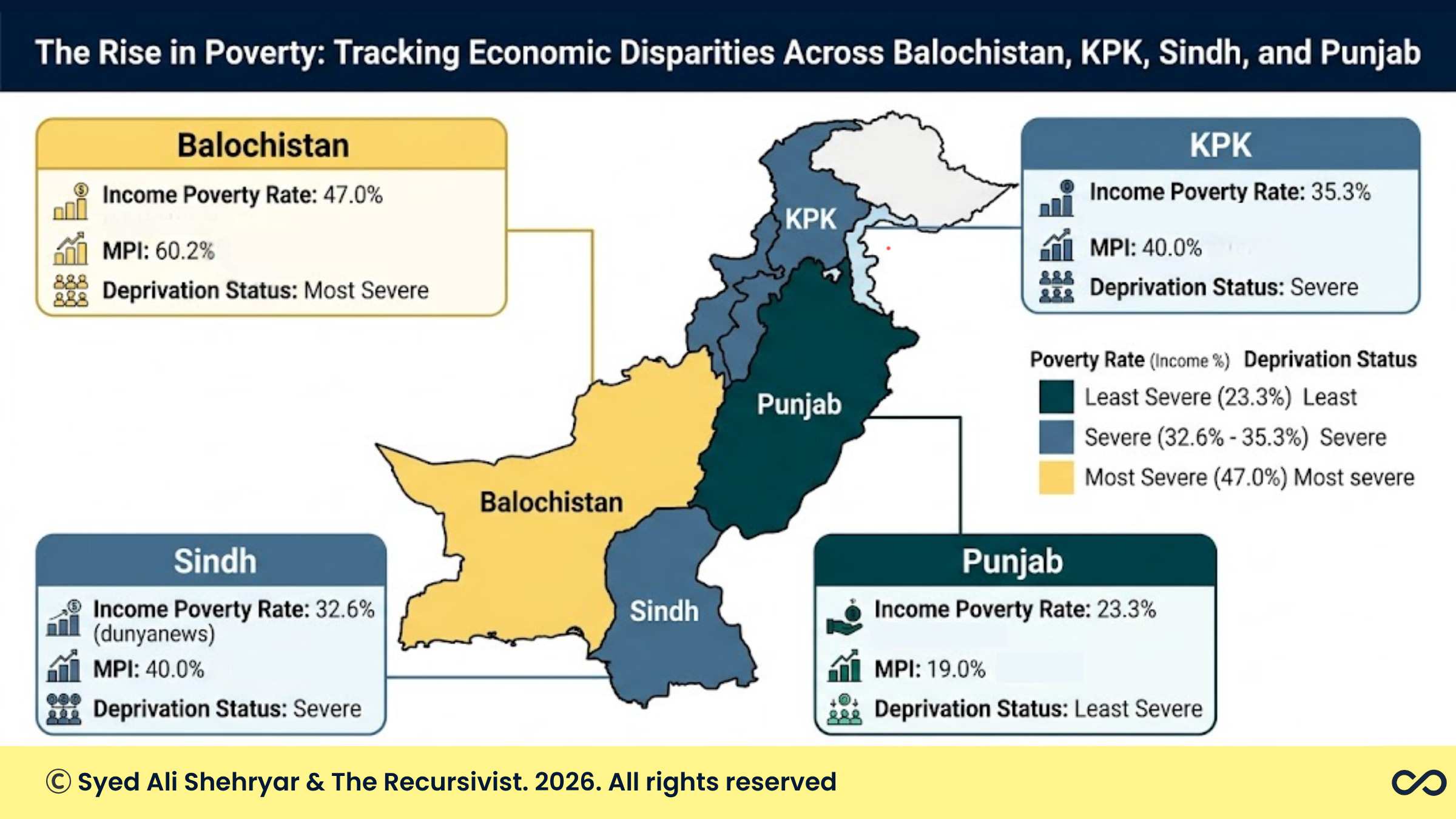

Pakistan’s poverty rate was already 29% before this hike. This is the highest in 11 years, up from 21.9% in FY19.

Rural poverty rose from 28.2% to 36.2% in a single year.

In Balochistan, almost one in every two people lives in poverty.

Households at this income level spend 40 to 50% of what they earn on food.

Petrol at Rs458 raises the price of flour, medicine, and construction materials, practically anything that moves by road. Nothing is insulated.

On the western border, Operation Ghazab Lil-Haqq has also increased the demand for diesel and aviation fuel. Those costs move with the same oil price shock that is pushing petrol to Rs458. Defence fuel bills and household fuel bills are rising from one source.

So defence and household fuel bills are both rising off the same external shock. The state is trying to run a war, meet IMF targets, and manage the streets on a revenue base that keeps failing. That is one binding constraint, not three separate issues.

Quiet Moves That Matter

The IMF has set 11 structural benchmarks for Pakistan through the end of 2026.

These are specific conditions around tax policy, spending, and reforms. If Pakistan misses too many of them, the IMF can pause or end the programme.

The petrol levy hike buys the government a little more apparent compliance on paper. It does not stop the benchmark clock. April revenue numbers will be the first under the Rs458 fuel price. If demand falls and imports drop, revenue from consumption and trade will fall. That will move Pakistan closer to a programme review point that it is not ready to pass.

The market is trading the fuel headline. It is not yet trading the risk that the benchmarks trigger a funding shock. That gap is where the more serious risk sits this week.

What This Means Now

People

The fuel hikes now line up directly against people who already have nothing left to cut.

Over the next one to three months, three expense lines move together.

Transport fares rise because bus and rickshaw owners cannot absorb Rs458 petrol.

Flour and other staples cost more because mills and trucks run on diesel that tracks the same oil prices.

Electricity bills go up because backup power for the grid still depends on furnace oil and RLNG, which are tied to global fuel prices and Gulf supply.

Unemployment stands at 7.1 percent and poverty has risen from 21.9 percent to 28.9 percent since FY19.

That means the shock lands on households that have already taken a large hit with no savings buffer.

The real medium term risk is not just a few hard months. It is a lasting drop in small savings and informal investment. That hits small shop openings, rural equipment purchases, and even remittance behaviour.

For a household, the practical move now is to write down all monthly bills under two cases.

One, fuel and power stay near current levels for six months.

Two, they rise again if Gulf supplies get tighter.

Any expense that cannot survive both cases without new debt is at risk and needs a plan.

Investors

For the next 60 to 90 days, a cautious strategy is to hold only short term positions that can be exited quickly, in names with mostly local cost and revenue, such as basic consumer goods. Avoid long term government bonds, banks with heavy exposure to public paper, and shares where earnings depend on state projects or cheap imports.

Businesses

Fuel is now the tax that runs through every business model.

Fuel costs that runs through logistics, generators, raw material transport, and staff commutes are squeezing exporters, especially in textiles, from both ends. Their input and freight costs are up, while buyers can shift orders to Bangladesh or Vietnam if Pakistani prices rise too much or if they worry about unrest.

Producers of chemicals, plastics, and medicines buy imported inputs that are often linked to oil and gas prices. They sell into a market where household demand is slowing. That means less room to raise prices without losing volume. At the same time, suppliers up the chain will push for tighter payment terms to cover their own cash needs.

For firms with Pakistan exposure, three moves stand out.

Reprice contracts where possible using a fuel cost clause or shorter price tenors.

Cut inventory cycles so less stock sits on shelves at old prices while costs move.

And review any capital commitment that assumes calm conditions around the June IMF review period.

Those plans carry more risk now.

Policy and Development Actors

Policy makers and aid agencies are now operating inside a very tight box.

The state is trying to fund cash transfers, some level of public projects, and a counterinsurgency, all while keeping the IMF on side. The gap in tax revenue, the use of the fuel levy, and the cuts to project spending show that there is no spare fiscal room left. The 11 IMF benchmarks through 2026 are a timer. If too many are missed, the programme can pause.

If the programme stalls, access to foreign exchange shrinks quickly. That affects fuel imports, medicine, and any field operation that depends on imported gear or services. It also affects Gulf and Chinese confidence in Pakistan as a partner.

For government and development actors, the practical move is to triage. Which programmes absolutely need state co funding in Q4 FY26, and which can be slowed without deep harm. Which reforms can realistically pass in the next three months, and which are fantasy under current political and social strain. This is not a quarter where every ambition can move forward together.

What to Watch Next Week

April CPI reading

Watch if headline inflation goes into double digits. The government projects 7.5 percent inflation for FY26.

The April figure will be the first after the full Rs137 hike feeds into prices.

A print above 10 percent would break that forecast and push the State Bank toward higher interest rates.

That would raise debt service costs and deepen the budget gap. It also gives the IMF reason to doubt the programme’s base case.

If inflation jumps, expect local bonds and PSX to reprice and the June IMF review to get rougher.

FBR April revenue data

April is the first month with Rs458 petrol fully in place.

If people spend less and trade volumes fall, tax collection will not match the pace needed to raise Rs4.672 trillion by June.

The revised Rs13.45 trillion target would then be out of reach.

If April numbers look weak, treat that as an early sign of programme stress, not a one month blip. Investors and firms with 90 day exposure should be ready to cut risk fast.

Security events tied to TTP and Operation Ghazab Lil Haqq

Each spike in fighting raises fuel and logistics costs just when households are already angry about prices.

If a major attack hits KP or Balochistan, where poverty is above 35 percent, in the same week that fuel pain and tax stories dominate the news, that is the mix that can turn scattered anger into organised street action.

That would raise the political risk that foreign lenders and investors use in their models and can shorten Pakistan’s external funding runway.

So what: Compared with last week, anyone with Pakistan exposure should shorten time horizons, cut positions that depend on state project spending, and read the fuel levy as hard proof that structural tax reform will not land before the June IMF review.

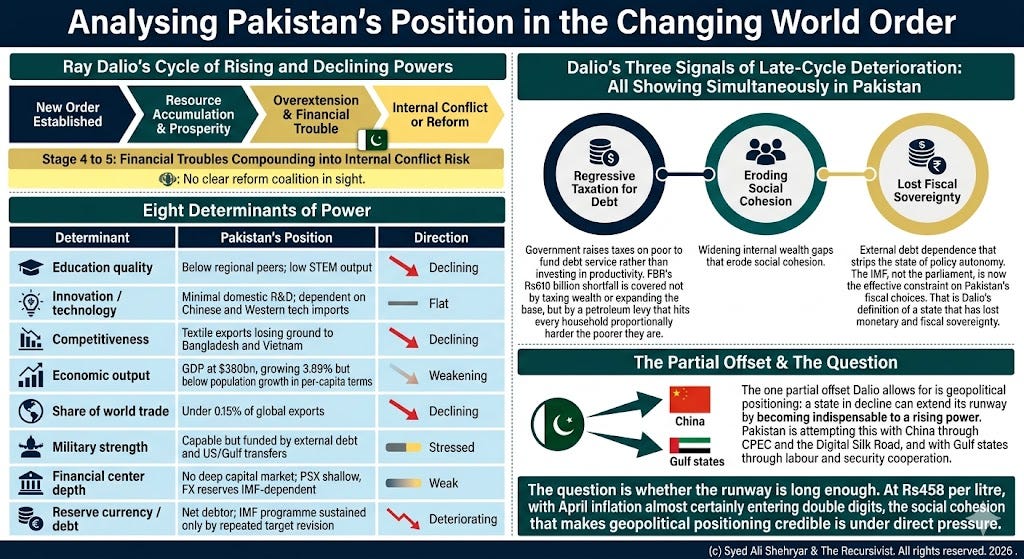

Interestingly, in Principles of Changing World Order, Ray Dalio tracks eight main strength markers for a country: education, competitiveness, innovation and technology, economic output, share of world trade, military strength, financial center strength, and reserve currency status. These tend to rise together in a good phase, then erode together when a country starts to slide.

Overall posture: Summed in the image below.

The petrol hike exposes Pakistan’s fiscal bleed. The next months will show whether the state keeps asking the same small group of people to pay for the same old failures, or whether anyone in power is finally ready to accept what the numbers are already saying.

Surviving week at a time and at the wits’ end

- Syed Ali Shehryar