Weekly Brief | Week of April 10, 2026

The rise of regional stabilizer: Pakistan averts a global catastrophe

Summary

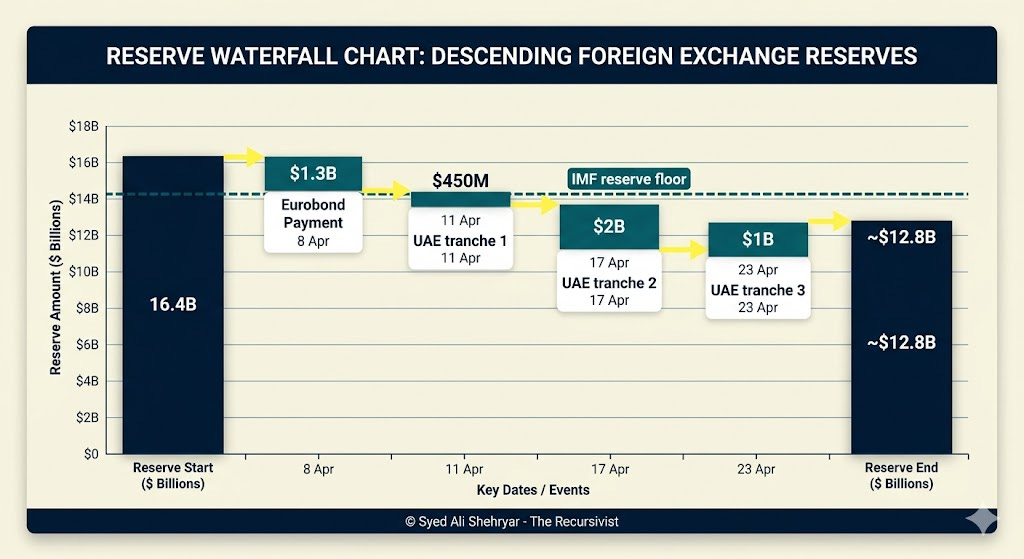

On Tuesday, Pakistan’s reserves stood at $16.4 billion. By 23 April, the government will have sent $4.8 billion out the door in debt payments, including $3.5 billion owed to the UAE and a $1.3 billion Eurobond that matured on 8 April. If no one replaces that money, reserves drop to roughly $12.8 billion, which falls below the floor the IMF requires.

This is happening in the same week Pakistan pulled off its most visible diplomatic win in years: brokering the US-Iran ceasefire.

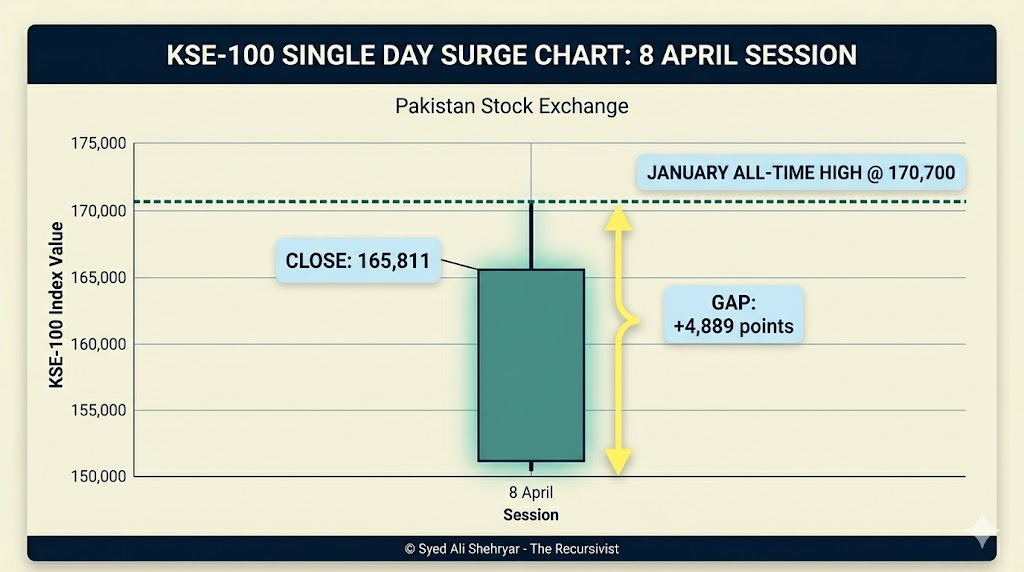

The KSE-100 surged 9.32% in a single session. Global oil risk fell. Islamabad earned a seat at the negotiating table it has wanted for decades.

The base case for the next 60 days

Pakistan's diplomatic standing buys goodwill and modest energy cost relief, but the reserve gap becomes the binding constraint within 30 days unless a bilateral partner steps in.

Bilateral financial flows, the $800mn Etisalat payment, and potential sanctions relief that could unlock the Iran-Pakistan gas pipeline. The main buffer is Pakistan's simultaneous credible access to both Washington and Tehran, which no other actor in the region currently holds.

The main buffer is that diplomatic standing itself, which strengthens Pakistan's hand in funding conversations.

The main vulnerability is the $3.5 billion hole in reserves for which the push would be for truce to hold long enough for the negotiation talks in Islamabad to produce a written framework, giving Pakistan a narrow window to convert diplomatic capital into concrete economic concessions.

What Changed

Pakistan's diplomatic footprint is structurally larger this week than last.

Last year, when Field Marshal Asim Munir held a one-on-one lunch with President Trump at the White House, it was the first time a sitting US president received Pakistan's military chief without civilian counterparts present.

Iran's President Pezeshkian called PM Shehbaz Sharif on March 28, praising Pakistan's "supportive role for peace." On March 29, the foreign ministers of Saudi Arabia, Egypt, and Turkey flew to Islamabad and produced a five-point peace plan calling for an immediate ceasefire and Hormuz reopening. FM Dar then flew to Beijing; China endorsed the effort and issued a joint statement. Israel removed Iran's Foreign Minister and Parliament Speaker from its assassination target list reportedly at Pakistan's request.

Pakistan is now functioning simultaneously across the US, Iran, Gulf Arab, and China diplomatic channels. India, by contrast, has been structurally sidelined. PM Modi's visit to Israel right before strikes began destroyed New Delhi's claim to neutrality. That shift in relative position is durable regardless of what happens to the ceasefire next week.

The ceasefire itself is under immediate strain, and the downside is sharp. Iran submitted a 10-point plan that includes retaining physical Strait of Hormuz control, excluding "unfriendly" flag states, imposing inspections, and charging fees which US has not agreed to, and which carries legal risks under UNCLOS. But the US also struck Kharg Island, handling roughly 90% of Iran's crude exports, hours before announcing the ceasefire. The trust deficit is likely to have enforced this as a non-negotiable.

CFR notes Iran now holds Strait leverage it did not possess before the war began

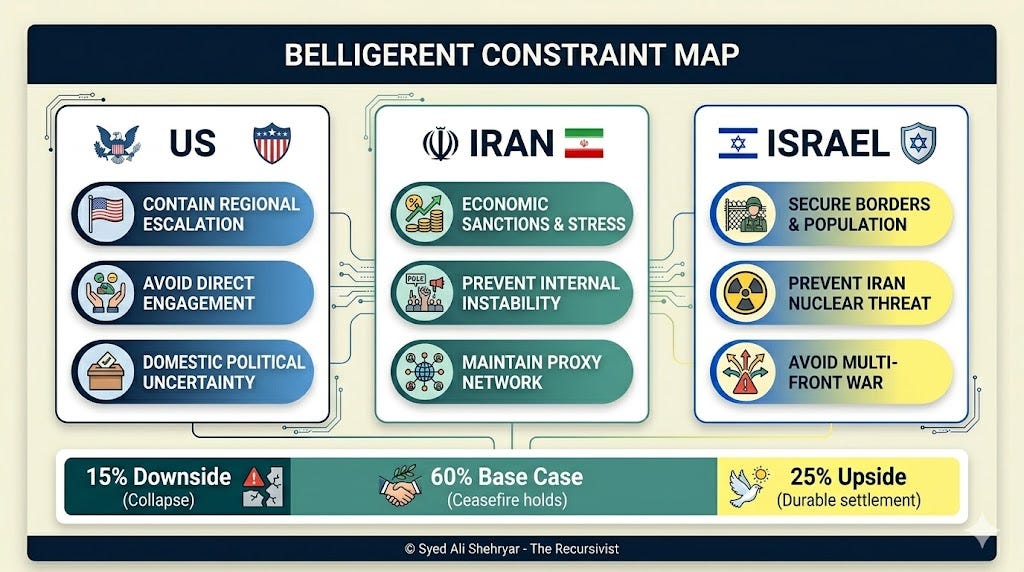

Nonetheless, the ceasefire is more likely to hold than not. And that is because all three belligerents are spent.

The US faces domestic war fatigue and a strategic pull toward China competition. The US has depleted ammunition stockpiles in the region and overestimated air power's ability to force regime change.

Iran’s layered sanctions and subsidy pressure at home make a prolonged fight unaffordable.

Israel’s long range strike capacity is stretched, and its domestic politics are strained.

Each side chose to pause because continuing costs more. That gives the ceasefire a roughly 60% chance of lasting three to five years. It remains reversible at any point.

Formal talks begin at Islamabad’s Serena Hotel on 11 April. VP JD Vance leads the US side, joined by Steve Witkoff and Jared Kushner. Iran has sent Parliament Speaker Ghalibaf and FM Araghchi. Vance’s visit makes him the first sitting US Vice President in Pakistan since Biden in January 2011.

Pakistan’s broker position rests on a specific mix. It comprises 900 km of shared border with Iran, the world’s second largest Shia population, Major Non-NATO Ally status since 2004, no US military bases on its soil, and a direct White House channel that opened after the Pakistan-India standoff in May 2025. That combination lets Pakistan talk credibly to the US, Iran, Gulf states, and China at the same time.

Before the ceasefire, the Strait of Hormuz was effectively closed. On 1 and 2 March, zero ships passed through. MSC, Maersk, CMA CGM, and Hapag-Lloyd pulled out entirely. Flow dropped more than 90%. Roughly 10 million barrels per day of oil went offline. DP World shut down Jebel Ali after interception debris started a fire. Emirates SkyCargo, KLM, and Turkish Airlines suspended Gulf flights. Both air and sea freight through Dubai stopped at the same time for the first time in the city’s modern history.

This consequential yet structural decline of the UAE has opened real competitive space for Pakistan that was not available 30 days ago. UAE saw a 51% reduction the volume of property transactions (deal count) since March 28 when attacks on Iran began. Prices fell 4-7%. US financial institutions (CITI, Goldman Sachs) shut their physical operations in the UAE. Gold was trading at a $30/oz discount in Dubai as capital flees. On 28 March, Iranian strikes hit Emirates Global Aluminum’s smelter in Abu Dhabi and Aluminum Bahrain’s facility. EGA reported damage that will take 12 months to repair. Six workers were injured. These are hits to productive assets that will take quarters to restore even with the ceasefire in place.

More durably, IMEC, the India-Middle East-Europe Economic Corridor announced in September 2023, has been effectively neutralised. Saudi Arabia conditioned participation on Palestinian statehood, UAE infrastructure is now war-damaged, and Israel is globally isolated. IMEC was the one geopolitical infrastructure project capable of permanently locking in India's alternative corridor advantage over Pakistan. Its collapse removes that threat from the next planning horizon.

Pakistan's bilateral position with the UAE has also shifted. The UAE bilateral loan will soon be repaid, removing Abu Dhabi's primary financial coercion instrument over Islamabad at precisely the moment the UAE's own bargaining power is at a cyclical low.

While all this was happening, Pakistan, notably, was the first country (other than China and India-bound vessels) to cross Hormuz after the closure. A Pakistani oil tanker crossed on 16 March with Iranian permission. Malaysia followed on 26 March. A French ship crossed on 3 April.

That crossing was small in tonnage. Its signal was large. Iran treated Pakistan as a trusted neutral.

Interesting signals that matter

Remittances fell 5% year on year in March, from $4.054 billion to $3.831 billion. The drop coincided with Gulf flight suspensions and port closures that disrupted worker and money flows. If this recovers as the Gulf normalizes, it was a blip. If it reflects workers leaving or remittance channels shifting away from Pakistan, the annualized loss runs $2 to $3 billion in foreign exchange inflows. That tightens the reserve position right when the UAE repayment is already draining it.

The KSE-100’s one day 9.32% surge (closing at 165,811, near its January all-time high of 170,700) shows that markets have priced in a peace dividend ahead of any fiscal confirmation. March inflation ran at roughly 7 to 7.3% year on year, above the State Bank’s 5 to 7% target. The SBP held its policy rate at 10.5%.

Hapag-Lloyd and MSC are actively rerouting or suspending Gulf-bound services, and DP World (which operates Jebel Ali) has opened emergency land corridors into Saudi Arabia to handle diverted cargo. For Pakistan, this is an opportunity. If major carriers treat Jebel Ali as a risk zone for the next 12-24 months and Pakistan takes no action to accelerate Gwadar's commercial throughput capacity or address Balochistan's political instability, that window closes without Islamabad capturing any diverted trade flow.

Pakistan is formally demanding the $800mn Etisalat payment while the UAE's negotiating power is at its weakest point in years. If Pakistan collects while this leverage window is open, it strengthens reserves without touching the external bond market. Every month of delay risks UAE financial actors recovering faster than property-crash data implies.

What This Means Now

People

Lower oil risk reduces the probability of fuel, electricity, and food price spikes over the next one to three months. If Hormuz stays open and oil prices stay down, inflation should ease toward the SBP’s target band.

The question for households: does the government use this breathing room to cut energy circular debt (the system of unpaid bills between power companies and the government that eventually shows up in everyone’s electricity tariff), or does it pass the benefit through as cheaper fuel? For the roughly 9 million Pakistani households that rely on Gulf remittances, any sustained disruption to worker flows hits daily budgets directly. The March dip deserves close attention.

Investors

The SBP policy rate sits at 10.5%. April debt service totals $4.8 billion against $16.4 billion in reserves. When the UAE’s $3.5 billion deposit leaves and if no bilateral partner (Saudi, Chinese, or other) replaces it, reserves breach the IMF floor and the programme faces complications.

Two separate forces are at work here.

The global force: lower Gulf war premiums, cheaper oil, and improved risk appetite across emerging markets help Pakistan passively, the same way they help every other frontier economy.

The local force: whether Islamabad uses this window to push through the IMF’s 11 structural benchmarks (tax reform, state owned enterprise cleanup, trade liberalization, special economic zone policy) determines if the external relief compounds or evaporates once global premiums tick back up.

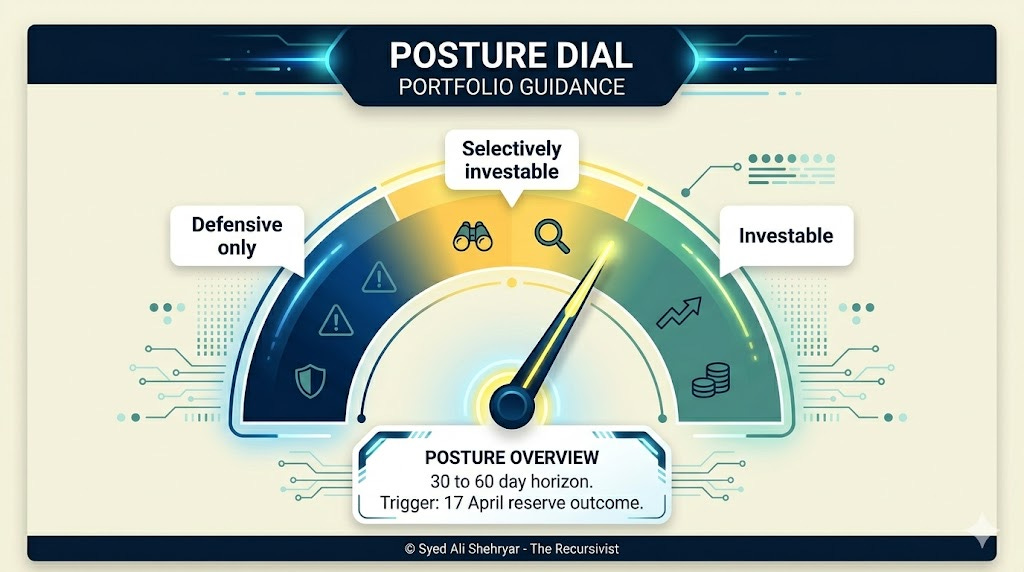

Rational positioning: hold current exposure, do not add until the UAE deposit question resolves by 17 April, and hedge any new rupee positions against the reserve floor breach scenario. Bank equities, IT exporters, and short duration government paper remain the rational sectors. Avoid long duration rupee bonds and anything with direct Hormuz logistics dependence until insurance and surcharge costs clear.

Businesses

The immediate operational signal is that energy costs and logistics disruption risk have stabilised, but not resolved. CMA CGM reopened Gulf bookings on 11 March using overland routes. Saudi Aramco pushed Red Sea pipeline contingencies, with Yanbu becoming an alternative crude loading point. Jebel Ali resumed operations with booking restrictions through late March. War risk surcharges and elevated insurance premiums have not fully cleared.

For import dependent manufacturers and Gulf route exporters, operating costs remain higher than pre-war levels. CPEC Phase II (21 MOUs, roughly $8.5 billion) benefits from reduced country risk under the ceasefire, but the IMF’s structural benchmarks on state owned enterprise restructuring and special economic zone policy create regulatory uncertainty for contracts in those corridors.

Policy and development actors

Three constraints eased this week that did not ease last week: the UAE bilateral loan will be repaid; IMEC's neutralization removes India's corridor-competition pressure; and Pakistan has unprecedented simultaneous access to the US, China, Iran, and Gulf Arab states. Pakistan’s broker status gives it a stronger hand in IMF review discussions and multilateral lending conversations. The 11 new benchmarks create a tight reform window.

The Saudi Strategic Mutual Defence Agreement and CPEC Phase II MOUs show Pakistan locking in obligations to multiple partners at once. That gives it bargaining power and creates obligations that reduce future policy flexibility. Meanwhile, Transparency International Pakistan flagged on 9 April that the $800 million owed from the 2005 PTCL privatization (Etisalat/e&) has accumulated to roughly $6 billion in penalties, sitting uncollected while the government borrows at high cost.

The binding constraints that did not ease are inflation above the SBP target band, GDP growth too weak to broaden PSX gains beyond banks and a few large conglomerates, and a domestic sectarian fault line that limits how far the civil-military leadership can publicly commit to either side of the US-Iran divide without triggering protests with real fiscal and security costs.

The Iran-Pakistan gas pipeline is the single biggest structural energy fix available to the country and requires a dedicated cross-ministry task force now, while a sanctions-relief window may be opening in the Islamabad talks.

Any fiscal dividend unlocked by ceasefire-driven goodwill must be directed at infrastructure, tax-net expansion, and energy investment, not short-term consumption relief, or the window will produce a sugar high with no lasting structural change.

What to Watch Next Week

UAE deposit replacement. The first $450 million tranche falls on 11 April, with $2 billion on 17 April and $1 billion on 23 April. If no bilateral partner (Saudi, Chinese, or other) announces a replacement deposit by 17 April, reserves breach the IMF floor. Watch also for early signals: Gulf sovereign wealth fund liquidity allocations shifting away from Pakistan linked bonds would indicate the deposit gap will not be covered.

Ceasefire durability. Vance and Ghalibaf sit down on 11 April. Lebanon is the fault line: Israeli strikes on 8 April killed over 200 people, and Araghchi warned Tehran could walk away if strikes continue. If the talks produce a framework or extension, Pakistan's broker premium holds. If Lebanon triggers an Iranian exit, oil spikes and the peace dividend disappears.

Remittance recovery. March fell 5% year on year. April data (available mid-May) will show whether this was a logistics disruption or a structural shift. Gulf airline and port normalization rates are a leading indicator. If remittances stay below $3.8 billion for a second month, the SBP's current account assumptions need revision.

Etisalat $800mn payment: demand confirmed or delayed. Any public confirmation that Pakistan has formally initiated legal or diplomatic proceedings to recover the $800mn Etisalat outstanding payment, or alternatively a UAE signal of refusal or extended delay. Why it matters: Successful collection is a direct FX reserve positive without external bond issuance at a moment when Pakistan's leverage over the UAE is at a cyclical high. Delay or refusal would signal that UAE financial actors are recovering faster than the property-crash data implies, and would require revision of the "UAE leverage permanently reduced" thesis that underpins part of the bullish Pakistan positioning case.

Posture

Compared with last week, a rational person with Pakistan exposure should hold positions rather than add, treat 17 April as a binary trigger on the reserve question, and hedge new rupee exposure against the possibility that reserves breach the IMF floor.

Overall posture: Pakistan is selectively investable for the next 30 to 60 days, which means a rational investor should maintain net Pakistan exposure and focus on bank equities, IT exporters, and short duration government paper, while avoiding long duration rupee bonds and any sector with direct Hormuz logistics dependence until insurance and surcharge costs normalize.

Confidence Note

Taken together, the strongest signals this week are Pakistan's confirmed dual-channel access to both Washington and Tehran (Munir-Trump lunch; Pezeshkian-Sharif call; Saudi-Egypt-Turkey FMs in Islamabad), the UAE's structural weakening at a moment Pakistan holds zero bilateral debt leverage from Abu Dhabi, and the PSX's 9.32% single-day re-rating on falling Gulf-risk premium, so the base case is that Pakistan has entered a 90-day window of elevated diplomatic and financial leverage it has not held since the early 1970s.

The base case: Pakistan earns a modest diplomatic and energy cost uplift and faces a tight 30 day window where reserve adequacy becomes the binding constraint.

If this view is wrong, it is most likely because the ceasefire collapses before the Serena talks produce a framework (triggered by continued Israeli strikes on Lebanon and an Iranian walkout), which would push oil back above $100, force SBP tightening, and throw Pakistan’s IMF programme into emergency review, raising imported inflation by 3 to 5 percentage points within a quarter.

For the next 30 to 90 days, risk is skewed to the downside for importers and consumers (energy cost reversal if the ceasefire breaks), roughly balanced for investors (market optimism set against fiscal fragility), and modestly to the upside for policy actors, provided they convert diplomatic standing into concrete funding before the window shuts.

If the deposit gap is filled by 17 April and the Serena talks produce even a procedural extension, Pakistan enters May with the strongest diplomatic hand it has held in a decade and just enough reserves to keep the IMF programme alive. If either fails, the ceasefire becomes a line item in the history books, and the fiscal math takes over.

Pakistan's geography has always been its destiny — this week, for the first time in a generation, its leadership chose to use that geography rather than be used by it; if the state can now convert one extraordinary week of diplomatic audacity into five years of institutional deepening, the regional re-rating will become permanent rather than a single extraordinary session on the exchange.

— Syed Ali Shehryar