Pakistan's Real Estate Tokenization

A guide to PVARA and what does this tokenization mean for the sector

Pakistan recently gave virtual assets a legal home. The Pakistan Virtual Assets Regulatory Authority, or PVARA, now sits inside the government’s financial management juggernaut, the Finance Division, with a board that includes the Secretaries of Finance and Interior, the State Bank of Pakistan (SBP) Governor, and the Securities and Exchange Commission of Pakistan (SECP). For a country that spent years effectively banning crypto, this is a real shift.

I recall a line by a friend and colleague who worked on regulatory reforms globally: A regulator on paper is not a market in practice. Over here, PVARA exists as a legal entity but the actual machinery that would make tokenization work for investors, specifically the banking connection between rupees and crypto platforms, is not yet in place.

If you’re thinking that Pakistan opening up to virtual assets might assume the market is open. It is not. There is a gap between the announcement and the working system.

Understanding Real Estate Tokenization

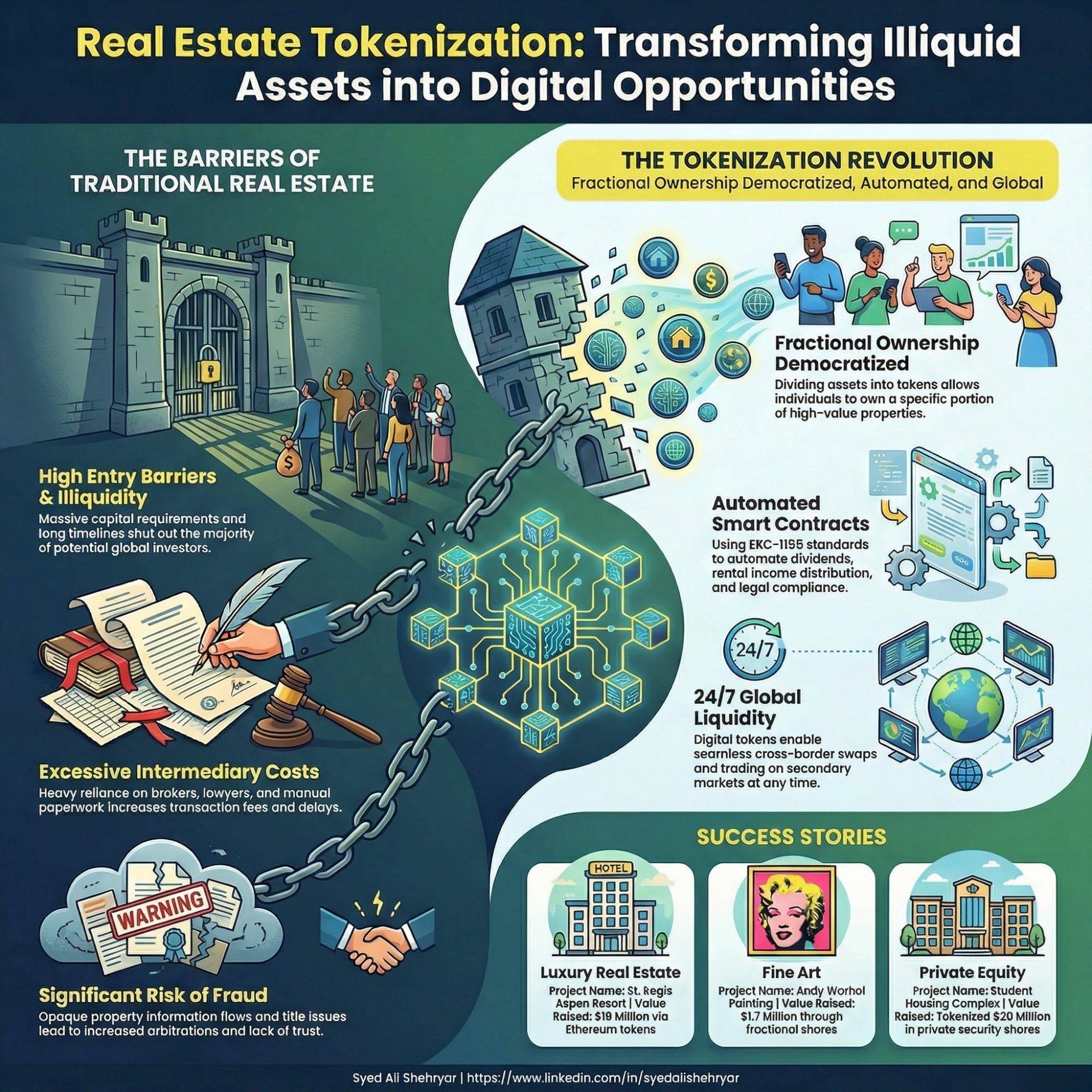

Real estate tokenization turns a physical property into digital tokens recorded on a blockchain. A blockchain is a shared record book that no one controls and no one can alter after the fact. Each token represents a fractional ownership right in that property. Buy ten tokens in a commercial building in Islamabad and you are entitled to your proportional share of rent and any gain in value. A smart contract, a piece of code that runs automatically, distributes those payments without anyone writing a check.

The legal vehicle holding the property is called a Special Purpose Vehicle, or SPV. Tokens represent shares in that SPV. Legal documents are stored via IPFS, the InterPlanetary File System, a decentralized storage system linked directly to the smart contract. (Whether a Pakistani court would recognize that chain of ownership remains an open question.)

What’s The Hurry?

Pakistan’s government has a point to prove. It needs to live up to its claims of salvaging the economy and ensuring its “economic revival”. With two years completed and three remaining, it’s trajectory is significantly off-track.

Therefore, the motivation is fiscal.

While I am skeptical, figures cited in recent industry discussions put somewhere between $20 and $25 billion in the crypto wallets of Pakistani citizens, outside the banking system and beyond the reach of the tax authority. Separately, data from Chainalysis cited in those same discussions puts Pakistan's crypto wallet user base at 30 to 40 million people, compared to roughly 400,000 investors on the Pakistan Stock Exchange (PSX). That means roughly an investment of $700-$1000 per user on average in crypto investments.

The government cannot tax what it cannot see. Whereas every PSX transaction is automatically taxed, crypto trades aren’t. I’m against CGT anyways, given the government doesn’t waste any instance of squeezing every cent out of its citizens without giving much in return. Nonetheless, it has to do what it has to do. And now, that’s why they have made PVARA. Largely, as a mechanism to pull that money into the formal system.

Pakistan's real estate market also holds an enormous amount of wealth that moves slowly.

Tokenization, if it works, makes property closer to a tradeable stock. Overseas Pakistanis can, for example, buy a fractional stake in a Lahore apartment without flying back to sign paperwork. Developers get funding faster to complete the otherwise stalled or failing projects. Retail investors with limited savings get access to asset classes that were previously out of reach.

The government frames this as widening access for ordinary investors. The early reality will likely be different. Overseas Pakistanis with foreign currency face no banking bottleneck and are best placed to buy in first. Local retail investors still cannot move rupees onto a licensed platform. More buyers in a market with limited supply pushes prices up. The people the government says it is helping may be the last ones who can afford to participate.

Regulatory Challenges

State Bank of Pakistan

The State Bank of Pakistan (SBP) controls whether commercial banks can send money to crypto platforms. PVARA can issue a license, but without a banking connection, that license has no working on-ramp for local investors. This has been the core tension.

The government’s approach separates the two roles.

SBP focuses on a Central Bank Digital Currency, a state-issued Digital Rupee for payments.

PVARA regulates private virtual assets as an investment class, separate from legal tender. Crypto becomes an asset to be regulated, not a currency to be tolerated. This framing helps SBP maintain its grip on monetary policy.

Treating tokenized real estate as an investment product rather than a payments instrument makes SBP’s cooperation more politically achievable.

The board structure makes this concrete. The SBP Governor sits on the PVARA board, giving the central bank direct oversight rather than leaving it to issue contradictory statements from outside.

However, stablecoins still remain an unresolved problem, and a point of contention between SBP and PVARA.

Dollar-backed stablecoins blur the line between asset and currency since you can use them for both. And SBP’s concern about effective dollarization means that category will stay restricted longer than others.

Ownership Dilemma

Tokenization requires a single, undisputed ownership record as its foundation. The blockchain is only as reliable as the property record underneath it. If the underlying title is in court, the token is worthless.

Before any property can be tokenized, the issuer must provide a clean title, a valuation report, and an information memorandum to SECP or PVARA.

That forced verification makes title disputes surface before investors are involved, unlike the traditional market where they typically surface after the sale.

Pakistan's land records outside a few urban centers are not digitized or clean enough to support a broad rollout.

Islamabad is the preferred starting point because Capital Development Authority, or CDA, properties are more centralized and better recorded than those in most provinces. One company is already operating in the SECP sandbox with a specific CDA-sector apartment submitted for approval. A national retail rollout is not close.

Islamabad is where this starts. Getting licensed to operate there is a separate question.

The Licensing Process

The Virtual Assets Ordinance 2025 sets out a three-phase process for any exchange or tokenization platform wanting to operate in Pakistan.

Phase one

Apply for a No Objection Certificate from PVARA, which requires a detailed business plan and corporate documents.

Phase two

Incorporate a subsidiary in Pakistan under the Companies Act 2017 and register with the Financial Monitoring Unit for Anti-Money Laundering compliance.

Phase three

Apply for the full Virtual Asset Service Provider, or VASP, license. This requires a Fit and Proper assessment of directors and lead personnel, proof of minimum paid-in funding specific to your license category (exchanges, custody services, and brokerages carry different thresholds), a physical office in Pakistan, and at least one senior person resident in the country.

Once licensed, you must hold customer assets in segregated accounts, maintain a cybersecurity framework and a business continuity plan, and run full Anti-Money Laundering and Know Your Customer programs.

The sandbox option lets new models test under supervisory oversight for up to 18 months before full commercial rollout, giving regulators time to observe compliance before opening the market fully.

Probable Outcomes

Two outcomes are more probable than the government’s stated ambition.

The first is bureaucratic stall: PVARA issues licenses, SBP keeps banking channels cautiously closed, and the market stays partly informal.

The second is state-led use: the government uses tokenization primarily to sell strategic holdings to large institutional buyers abroad, while retail access stays limited. With the WLF officials flying in an out frequently, this is what I’m closely tracking.

What Do Experiences Teach?

Developing economies with high inflation, money controls, and weak rule of law that pursue state-led digital asset adoption fail to reach mass adoption roughly 70% of the time.

Venezuela’s Petro and Zimbabwe’s gold tokens are the reference cases.

Pakistan’s organic crypto user base pulls the probability in a better direction. But structural friction pulls it back.

Realistically, if executed well, my reading puts broad retail success at around 35%, with a controlled market serving institutional and sovereign purposes first being the more probable near-term outcome.

If I were to track the signals that would make the real estate tokenization policy a success, I would concentrate on three tests:

If SBP issues guidance which explicitly allows banks to transact with PVARA-licensed platforms, its a signal that market will move. Silence from SBP means stall, regardless of what PVARA says.

Watch who gets the first licenses. If they go to politically connected conglomerates rather than independent fintech companies, retail access is not real yet.

If a participant completes the process cleanly and generates secondary market trading volume, the infrastructure works. If early projects stall or get quietly closed, push your timeline out by at least two years.

Until these conditions are met, I am considering the tokenization policy the same way I am considering the Space Policy, the Digital National Policy, and scores of others I have seen during my time at the Prime Minister’s Office - a bet that likely fails execution.